What is non employee compensation on 1099-Misc?

Ava Robinson

Published Mar 24, 2026

Nonemployee compensation (also known as self-employment income) is the income you receive from a payer who classifies you as an independent contractor rather than as an employee. This type of income is reported on Form 1099-MISC, and you’re required to pay self-employment taxes on it.

What happens if you do not report a 1099-Misc?

Generally, the penalty is $50 per 1099-MISC for not filing by the 2018 due date. The penalty increases to $100 if the form is not filed within 30 days of the due date and $260 after August 1, 2018. The maximum penalty for small businesses is $532,000, so this is not a reporting requirement to be taken lightly.

Where do you show non employee compensation on 1099-MISC?

Non-employee compensation appears on line 7 of Form 1099-MISC.

Where to report nonemployee compensation on Form 1099?

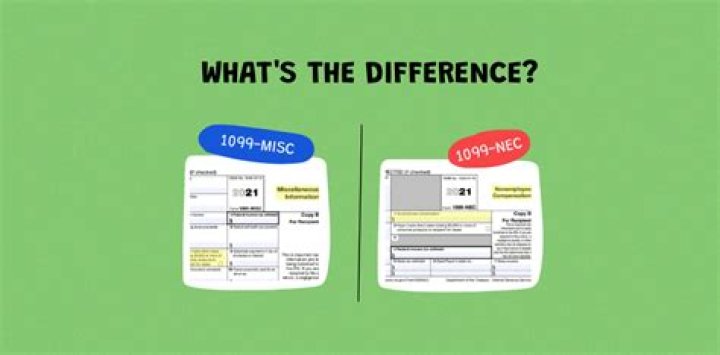

Nonemployee compensation for years has been reportable on line 7 of Form 1099-MISC, but beginning with 2020 forms, filers instead will report nonemployee compensation on Form 1099-NEC. This change, we are told, is designed to “increase compliance.”

When to send a 1099 MISC to a non employee?

The 1099-MISC form is for non-employees presenting the payment amounts during the year. In certain cases, there is no withheld taxes and no FICA tax withholding. If you are issuing the 1099-MISC form to a non-employee, it should be submitted to him or her by January 31st of the following tax year.

What kind of income can be reported on a 1099-MISC?

Independent contractor earned income but not an employee. Commissions, rents, fees or royalties paid. Payment made for awards, prizes or legal service. Before receiving a 1099-MISC form a non-employee must complete the W 9 Form, which is similar to W4 form that every employee completes during the hiring process.

Is the form 1099-nec a single use form?

This change, we are told, is designed to “increase compliance.” Unlike the catch-all that is Form 1099-MISC, Form 1099-NEC is a single-use form, reporting only nonemployee compensation, as well as taxes withheld from the payments, if any.