What happens if the costs are not allocated?

James Williams

Published Feb 19, 2026

When costs are allocated in the right way, the business is able to trace the specific cost objects that are making profits or losses for the company. If costs are allocated to the wrong cost objects, the company may be assigning resources to cost objects that do not yield as much profits as expected.

Why costs must be allocated?

Cost allocation is the assigning of a cost to several cost objects such as products or departments. The cost allocation is needed because the cost is not directly traceable to a specific object. The goal is to reduce the arbitrariness by identifying the various root causes of the overhead costs.

What are the three bases of cost allocation?

There are three types of allocation bases in Cost accounting:

- Predefined dimension member allocation bases.

- Hierarchy allocation bases.

- Formula allocation bases.

How do you calculate allocated cost?

How to Calculate Overhead Allocation

- Add up total overhead.

- Compute the overhead allocation rate by dividing total overhead by the number of direct labor hours.

- Apply overhead by multiplying the overhead allocation rate by the number of direct labor hours needed to make each product.

How is actual allocation base calculated?

What is basis of allocation?

Basis of Allotment or Basis of Allocation is a document publishes by registrar of an IPO to stock exchanges and IPO investors. This document provides information about final price fixed for an IPO, issue subscription (bidding) information or demand of an IPO and share allocation ratio.

What is the rule for selecting an allocation base for company expenses?

The allocation base should be a cause, or driver, of the cost being allocated. A good indicator that an allocation base is appropriate is when changes in the allocation base roughly correspond to changes in the actual cost. Thus, if machine usage declines, so too should the actual cost incurred to operate the machine.

How do you allocate cost?

Even Spread – Dividing IT costs evenly among business units is the easiest way to perform cost allocation. With this approach, IT cost data is simply split into equal parts. For example, a company might spend $1M on server maintenance each year.

Why must cost be allocated?

Cost allocation is used for financial reporting purposes, to spread costs among departments or inventory items. Cost allocation is also used in the calculation of profitability at the department or subsidiary level, which in turn may be used as the basis for bonuses or the funding of additional activities.

What are the disadvantages of allocation?

Allocating costs can sometimes lead to favoritism, where one department receives much more than the others if cost managers care for it more. This sort of bias can also cause a variety of related issues, such as infighting, bids for attention or inflation of department needs and ideas.

How do you allocate indirect costs?

You can allocate indirect costs by taking your total indirect expenses and dividing them by some sort of allocation measure, like direct labor expenses, direct machine costs, or direct material costs. The formula gives you a ratio. Let’s say that you want to find your overhead rate using your direct labor expenses.

Is any cost that is allocated to two or more cost objectives?

(b) After direct costs have been determined and charged directly to the contract or other work, indirect costs are those remaining to be allocated to intermediate or two or more final cost objectives.

What are the different types of cost allocation?

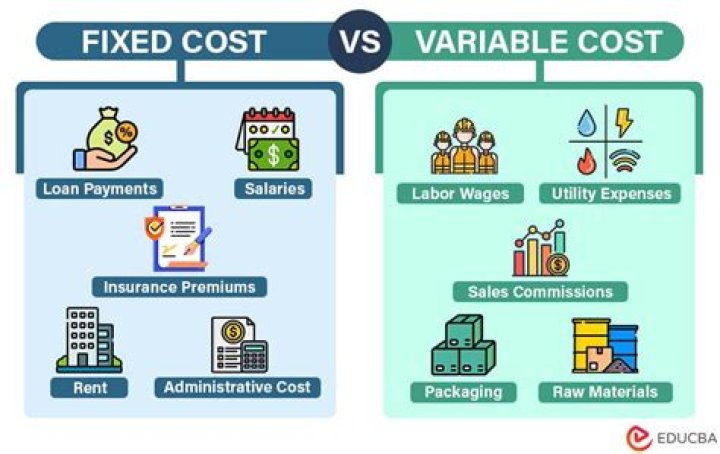

These costs include: 1 Direct costs Direct costs are costs that can be attributed to a specific product or service, and they do not need to be allocated to the specific cost object. 2 Indirect costs Indirect costs are costs that are not directly related to a specific cost object like a function, product, or department. 3 Overhead costs

Why do direct costs need to be allocated?

Direct costs are costs that can be attributed to a specific product or service, and they do not need to be allocated to the specific cost object. It is because the organization knows what expenses go to the specific departments that generate profits and the costs incurred in producing specific products or services

How are overhead costs allocated to cost centres?

Apportionment means sharing on a reasonable basis. Many overhead costs are costs that cannot be allocated directly to one cost centre, because they are shared by two or more cost centres. These costs are apportioned between the cost centres.