How do you record sales on credit?

Ava Robinson

Published Feb 28, 2026

To record early cash collections, businesses debit both the cash account and the account of sales discounts as an expense and credit accounts receivable to reduce the outstanding balance.

How do you record revenue received in advance?

When a company receives money in advance of earning it, the accounting entry is a debit to the asset Cash for the amount received and a credit to the liability account such as Customer Advances or Unearned Revenues.

What is the correct treatment of a sale on credit?

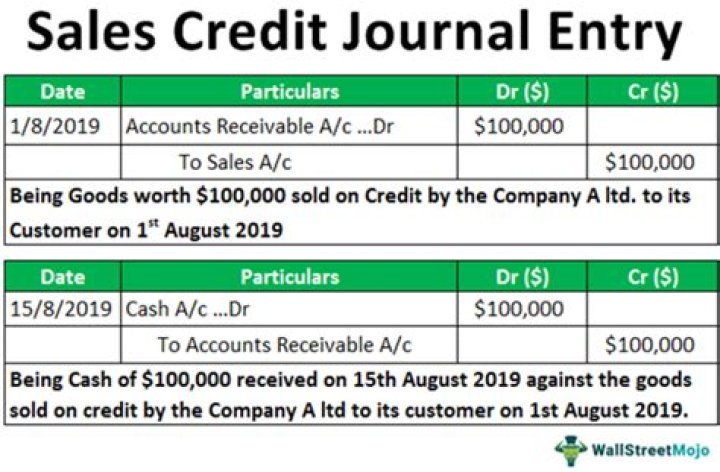

When the goods are sold on credit to the buyer of the goods, then the sales account will be credit in the books of accounts of the company. It will increase the revenue, and thus it will be shown in the income statement of the company in the sale period.

What is the journal entry for sales on credit?

The journal entry shows a $1,000 debit to accounts receivable and a $1,000 credit to sales revenue. To record a $1,000 sale — a credit sale — the journal entry needs to show both the $1,000 increase in accounts receivable and the $1,000 increase in sales revenue.

Is credit sales the same as sales?

In other words, credit sales are purchases made by are sales where the cash is collected at a later date. The formula for net credit sales is = Sales on credit – Sales returns – Sales allowances.

What are the credit terms for a credit sale?

Company A offers credit terms 5/10, net 30. If Michael pays the amount owed ($10,000) within 10 days, he would be able to enjoy a 5% discount. Therefore, the amount that Michael would need to pay for his purchases if he paid within 10 days would be $9,500.

When do you pay the seller on a credit sale?

Credit sales: Customers are given a period of time after the sale is made to pay the seller. 3. Advance payment sales: Customers pay the seller in advance before the sale is made. It is common for credit sales to include credit terms.

What’s the difference between cash sales and credit sales?

1. Cash sales: Cash is collected when the sale is made, and the goods or services are delivered to the customer. 2. Credit sales: Customers are given a period of time after the sale is made to pay the seller. 3. Advance payment sales: Customers pay the seller in advance, before the sale is made.

How much advance is received for future supply?

As per the explanation 1 to Section 12 of the CGST Act, 2017 a “supply” shall be deemed to have been made to the extent it is covered by the invoice or, as the case may be, the payment. For instance, an advance of Rs. 10 lacs is received for a supply worth Rs. 1 crore to be made in future.