Can I keep my 401k if I get laid off?

Mia Ramsey

Published Apr 12, 2026

Here’s what you can do with a 401(k) if you are laid off: Leave the money in your 401(k) if you have more than $5,000. Move the funds into an individual retirement account or 401(k) plan at a new job. Withdraw the funds and face potential penalties.

Can you contribute to 401k with unemployment?

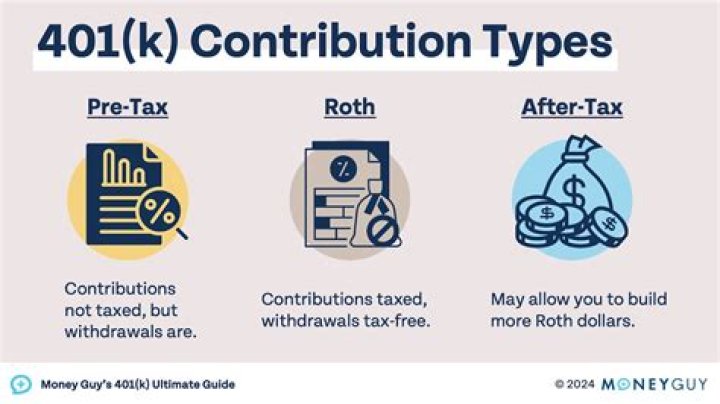

Legal Options With 401(k) You are legally permitted to contribute to your 401(k) at any time, whether you are employed, unemployed or retired. The account can remain with your old employer if you have at least $5,000 in the account.

If you are fired or laid off, you have the right to move the money from your 401k account to an IRA without paying any income taxes on it. This is called a “rollover IRA.” If they write the check to you, they will have to withhold 20% in taxes.

What happens to your 401k if you get laid off?

“These accounts are meant to be a vehicle for long-term retirement savings, so cashing out after a job loss can jeopardize your financial plan in the long run.” Using 401 (k) funds now to pay for immediate expenses could mean that later, when facing retirement, you don’t have that same amount available.

What happens to my 401k when I get a new job?

If you value the simplicity of having all of your retirement assets in one place—or you prefer the offerings of your new employer’s plan—you can roll your old 401 (k) into your next job’s 401 (k). Your old and new 401 (k) providers will probably have forms you can submit for an easy transfer between providers.

What to do with your retirement plan when you get laid off?

These days, layoffs are a fact of corporate life as companies try to grapple with economic cycles and global competition. One of the first choices laid-off workers face is what to do with their retirement plan assets.

What happens to my 401k If I file for bankruptcy?

If you file for bankruptcy, the implications for funds in a 401 (k) will not be the same as the consequences for an IRA. “Your 401 (k) cannot be included in a bankruptcy proceeding,” says Landon Loveall, a certified financial planner at KB Financial Advisors in San Francisco.