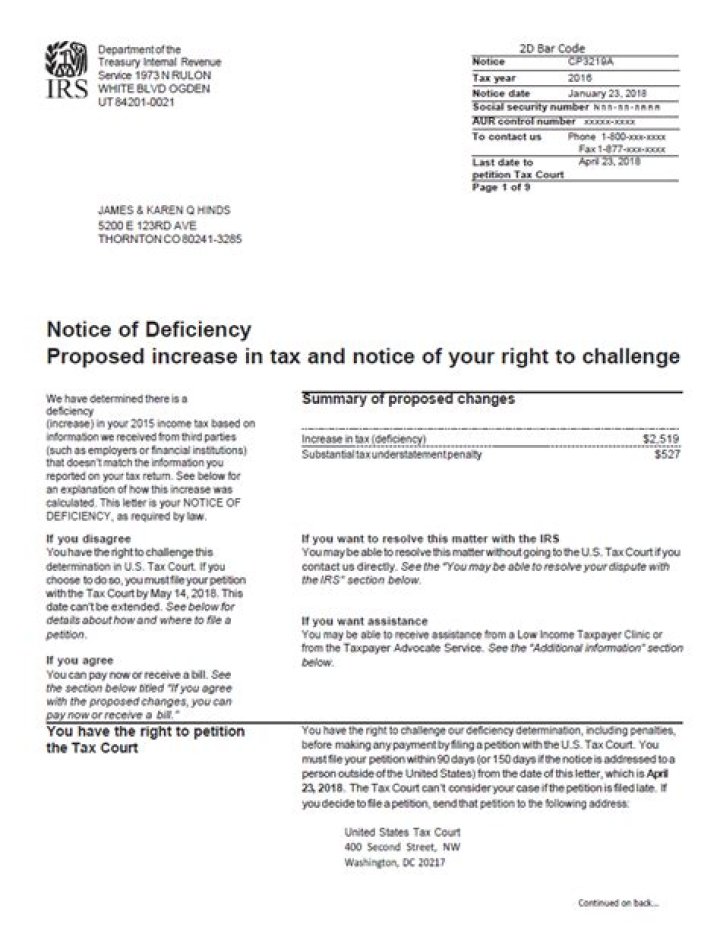

Why did I get a notice of deficiency from the IRS?

Henry Morales

Published Mar 22, 2026

A notice of deficiency is issued when the IRS proposes a change to a tax return because they found that the information reported on a return does not match their records.

What is the difference between a 90-day letter and a 30 day letter?

The 30-day letter asks the taxpayer to agree to the IRS’ findings. The 90 -day letter indicates a deficiency in tax. The taxpayer that wants to fight on can either pay the tax and sue for a refund in District Court, or file a petition for review in the Tax Court without paying the tax.

What penalties are deductible?

Fines and penalties a person owes to the government for violating local, state, and federal laws are never deductible. According to the IRS, the goal of its penalties is to discourage illegal activity related to federal taxes. Penalties also discourage people from neglecting their obligations to file or pay.

Why did I receive a CP11 notice from the IRS?

Why did I receive a CP11 Notice from the IRS? If you have received a CP11 Notice from the IRS, it usually means that the IRS believes there was a miscalculation on your tax return, that the IRS has made what it considers to be necessary corrections to your tax return, and that as a result of these changes, you now owe money to the IRS.

What happens if you miss the CP11 deadline?

When processing your return, the IRS discovered an error. The IRS corrected the error and made an adjustment to your return. This adjustment resulted in a balance due. If you miss the deadline: If you do not dispute the changes on a CP11 within 60 days, you must pay the balance due before the IRS will consider reversing the change. Want more help?

Where can I get help with my CP11 balance?

If you qualify for our assistance, which is always free, we will do everything possible to help you. Visit or call 1-877-777-4778. Low Income Taxpayer Clinics (LITCs) are independent from the IRS and TAS.

When to use CP11, math error on return?

A CP11, Math Error on Return – Balance Due, notice is issued when there is a mistake on your return that resulted in a balance due of five dollars or more. How did I get here?

One of the common reasons why the IRS issues a Notice of Deficiency is because income that was reported to them by a third party, like an employer or bank, was not included on the taxpayer’s submitted return. You want to compare the information in the letter with your tax return.

How long do you have to appeal an IRS Notice of deficiency?

You can challenge this discrepancy, but it’s important to note that you’ll only have 90 days to file an appeal. An IRS notice of deficiency is also often referred to as a “90-day letter.”

What happens after a notice of deficiency is issued?

Procedures covering what happens once the notice is issued are covered in IRM 8.2.2, Statutory Notice of Deficiency Cases. A notice of deficiency, also called a “statutory notice of deficiency” , “statutory notice” or “90 Day Letter” , is a legal notice in which the Commissioner determines the taxpayer’s tax deficiency.

When to file 90 day notice of deficiency?

These letters provide taxpayers with information about their right to challenge proposed IRS adjustments in the United States Tax Court by filing a petition within 90 days of the date of their notice (150 days if you reside outside the United States). This notice or letter may include additional topics that have not yet been covered here.

What does a 90 day notice of deficiency mean?

A Notice of Deficiency, also known as a Statutory Notice of Deficiency, Stat Notice, or 90-day letter, is the final notification a taxpayer will receive before the IRS makes its final assessment of tax due. The letter lets the taxpayer know how much additional tax the IRS is proposing and why.

How to return a notice of deficiency waiver?

Note: The amounts shown as due on the enclosed Form 5564, Notice of Deficiency – Waiver, may not match your previous notice amount due because you can’t challenge all items in U.S. Tax Court. You can return your response by mail or fax. The return address and fax number are on the notice.

When to issue notice of deficiency based on original returns?

See IRM 8.17.4.29.1 for further discussion of original returns when returns are filed electronically. However, if a statute is imminent, it may be necessary to issue a notice of deficiency based on copies of returns or a BRTVU/RTVUE. See IRM 8.17.4.29.1 for more information.

When do you receive a notice of deficiency?

You also may receive a statutory notice of deficiency if the IRS sent you one or more pre-assessment letters requesting income, credit, or deduction verification, but never received a response from you. Have questions about your Notice of Deficiency? We can help.

When to include IRC 6651 in a deficiency notice?

IRC 6651 addition (including the fraudulent failure to file penalty under IRC 6651 (f)) where such addition applies only to tax shown on a filed return. If the addition is applicable to a deficiency, show it in the notice.

Is there a notice of deficiency in IRM 8.17.4?

(1) Revised IRM 8.17.4.4 to reflect new Tax Computation Specialists (TCS) procedures for requesting preparation of a Notice of Deficiency.