Who may contribute to a Keogh plan?

Emma Jordan

Published Feb 26, 2026

Keogh plans are designed for use by unincorporated businesses and the self-employed. Contributions to Keogh plans are made with pretax dollars, and their earnings grow tax-deferred. Keogh plans can invest in securities similar to those used by IRAs and 401(k)s.

How much can I contribute to Keogh?

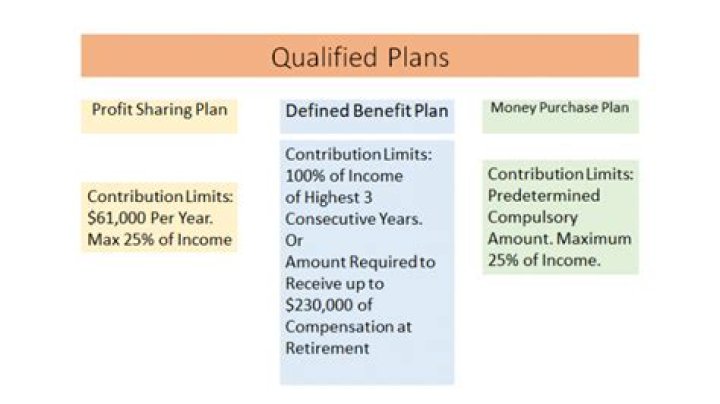

Keogh Plan Contribution Limits 2020 You can contribute up to 25% of compensation or $57,000. If you have a money purchase plan, you contribute the fixed percentage of your income every year. The contribution amount will come from the IRS formula.

What is a Keogh contribution?

Keogh plans are tax-deferred pension plans—either defined-benefit or defined-contribution—used for retirement purposes by either self-employed individuals or unincorporated businesses, while independent contractors cannot use a Keogh plan.

Can I contribute to IRA Keogh?

Can You Have Both a Keogh Plan and an IRA? Keogh plans can be established in addition to IRA accounts, but since a Keogh plan is a qualified plan, your contributions to your IRA account may not be fully deductible.

Do Keogh plans still exist?

While Keogh plans still exist today, they’re mainly used by highly compensated individuals because they offer high contribution limits. Unfortunately, the administrative burden of operating them can be substantial. Keogh plans can only be used by self-employed individuals and unincorporated businesses.

How much can you contribute to a Keogh Plan?

With profit-sharing, you can contribute up to $54,000 a year as of 2019, and you can deduct up to 25 percent of your income. The amount you choose to contribute to a profit-sharing plan can change each year. With a money-purchase plan, you determine at the outset the percentage of profits to be placed in the Keogh.

How does profit sharing work in a Keogh Plan?

The amount you choose to contribute to a profit-sharing plan can change each year. With a money-purchase plan, you determine at the outset the percentage of profits to be placed in the Keogh. But that contribution is required if there are profits and it can’t be changed. If the contribution isn’t made, you’ll face a penalty.

Can a self employed dentist contribute to a Keogh Plan?

A Keogh may be right for a highly paid professional, such as a self-employed dentist or lawyer, but the cases in which these plans make sense are specific and fairly rare. You define the contribution that will be made each year, and you can make contributions through profit-sharing or money purchase.

Do you need a financial advisor for a Keogh Plan?

It is one of the primary reasons that Keoghs can be complicated for the average self-employed individual. Talk to a financial or tax advisor before establishing a Keogh plan. The Balance does not provide tax, investment, or financial services and advice.