Who files a gift tax return the giver or receiver?

Sarah Duran

Published Mar 26, 2026

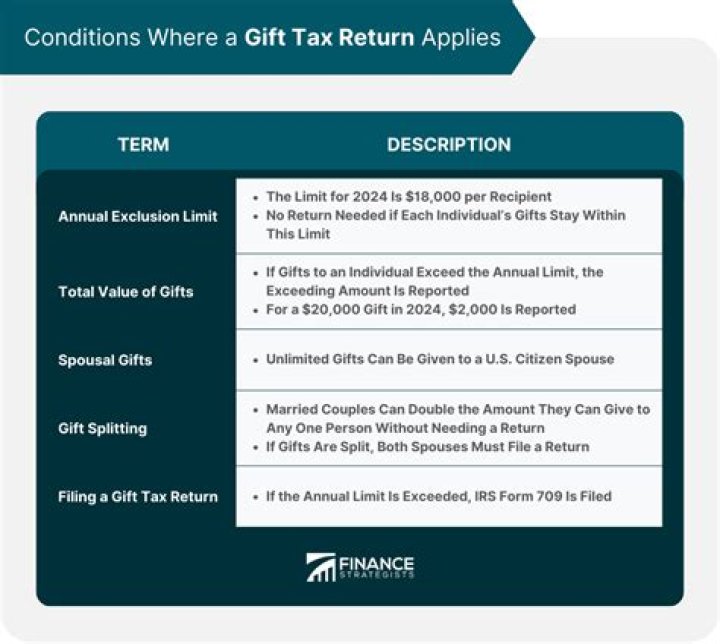

Generally, the answer to “do I have to pay taxes on a gift?” is this: the person receiving a gift typically does not have to pay gift tax. The giver, however, will generally file a gift tax return when the gift exceeds the annual gift tax exclusion amount, which is $15,000 per recipient for 2019.

Does the giver pay gift tax?

If you’re lucky enough and generous enough to use up your exclusions, you may indeed have to pay the gift tax. The rates range from 18% to 40%, and the giver generally pays the tax. There are, of course, exceptions and special rules for calculating the tax, so see the instructions to IRS Form 709 for all the details.

Gift tax is not an issue for most people The person gifting files the gift tax return, if necessary, and pays any tax. If someone gives you more than the annual gift tax exclusion amount ($15,000 in 2020), the giver must file a gift tax return.

How to fill out IRS Form 709 gift tax return?

You’ll need to fill out IRS Form 709 [pdf], “United States Gift (and Generation-Skipping Transfer) Tax Return”. The instructions are quite long and confusing. You ask your accountant and they suggest talking to your estate lawyer. You may wish to avoid paying the $400 an hour or whatever it will cost as the form should be pretty straightforward.

When do I not need to file Form 709?

All the gifts you made were of present interests”), it seems that I don’t need to file the form 709, since the gift is cash and was given to a relative. The gift meets all the three requirements. But at the other hand, the current lifetime gift upper limit is 5.45 millions.

When do you have to file gift tax return?

When taking the 5-year election, you must fill out the gift tax return (Form 709) by April 15th of the year following the year in which in the contribution was made. So if you make the contribution in 2018, you must file Form 709 by April 15th, 2019.

Do you have to pay GST on a transfer on Form 709?

Certain transfers, particularly transfers to a trust, that are not subject to gift tax and are therefore not subject to the GST tax on Form 709 may be subject to the GST tax at a later date. This is true even if the transfer is less than the $15,000 annual exclusion.