Which part of Circular 230 describes practice before the IRS and who is eligible?

James Williams

Published Apr 05, 2026

Any individual qualifying under paragraph §10.5(e) or §10.7 is eligible to practice before the Internal Revenue Service to the extent provided in those sections.

What does Circular 230 apply to?

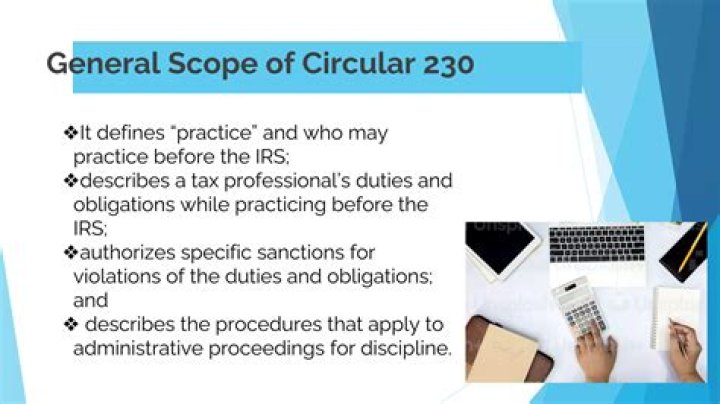

Circular 230 defines “practice” and who may practice before the IRS; describes a tax professional’s duties and obligations while practicing before the IRS; authorizes specific sanctions for violations of the duties and obligations; and, describes the procedures that apply to administrative proceedings for discipline.

What is the purpose of Circular 230 quizlet?

In determining the correctness of oral or written representations made by the practitioner to clients with reference to any matter administered by the IRS.

Who does Circular 230 apply to?

Who is subject to Circular 230 jurisdiction? State-licensed Attorneys and Certified Public Accountants (CPAs) authorized and in good standing with their state licensing authority who interact with tax administration at any level.

Is an individual required to file a tax return if he or she owes no tax quizlet?

Is an individual required to file a tax return if he or she owes no tax? Individuals who owe no tax because of deductions or other reasons must still file a return if they have gross income in excess of the filing requirement amounts. The normal due date for calendar year individuals and C corporations is April 15.

Does Circular 230 apply to unenrolled agents?

Also, unenrolled return preparers must comply with the rules of practice and conduct to exercise the privilege of limited practice before the IRS. There are two specific sets of rules that apply, both are contained in Circular 230: Duties and restrictions relating to practice (Subpart B of Cir. 230), and.

Who does IRS Circular 230 apply to?

What does Circular 230 say about practicing before the IRS?

Circular 230 defines “practice” and who may practice before the IRS; describes a tax professional’s duties and obligations while practicing before the IRS; authorizes specific sanctions for violations of the duties and obligations; and, describes the procedures that apply to administrative proceedings for discipline. Q3.

Who are the professionals covered by Circular 230?

The Office of Professional Responsibility (OPR) establishes and enforces consistent standards of competence, integrity and conduct for tax professionals, enrolled agents, attorneys, CPAs, and other individuals and groups covered by Circular 230. Circular 230 Tax Professionals | Internal Revenue Service Skip to main content

Who is liable for failure to comply with Circular 230?

• A responsible practitioner must take reasonable steps to ensure adequate procedures for compliance with Circular 230 are in place, and properly followed. –Liable for failure to take steps if violations occur, or –For failing to act if knew or should have known of violations Diligence as to Accuracy – § 10.22

What can a disbarred practitioner do for the IRS?

A suspended or disbarred practitioner can submit Form 8821 ( Tax Information Authorization) signed by a taxpayer to the IRS, authorizing the suspended or disbarred practitioner to obtain copies of the taxpayer’s tax returns and transcripts of account from the IRS.