Which of the following investment securities are not reported at fair value in the balance sheet?

James Williams

Published Feb 16, 2026

Which of the following investment securities are not reported at fair value in its balance sheet? Debt securities held to maturity. Refer to the process of allocating the cost of long-term assets used in the business over future periods.

Can you sell Held to maturity securities?

It is normally rare to transfer or sell securities that are classified as Held-to-Maturity (HTM). However, there are certain safe harbor rules available that permit the transfer or sale of HTM securities without tainting the portfolio or one’s ability to use this classification going forward.

Which of the following is the investment classification for which the investor’s positive intent and ability to hold is important?

The investment category for which the investor’s “positive intent and ability to hold” is important is: Securities classified as held to maturity.

What is held-for-trading?

A held-for-trading security is a debt or equity investment that investors purchase with the intent of selling within a short period of time, usually less than one year. Within that time frame, the investor hopes to see appreciation in the value of the security and sell it for a profit.

How are held to maturity securities reported?

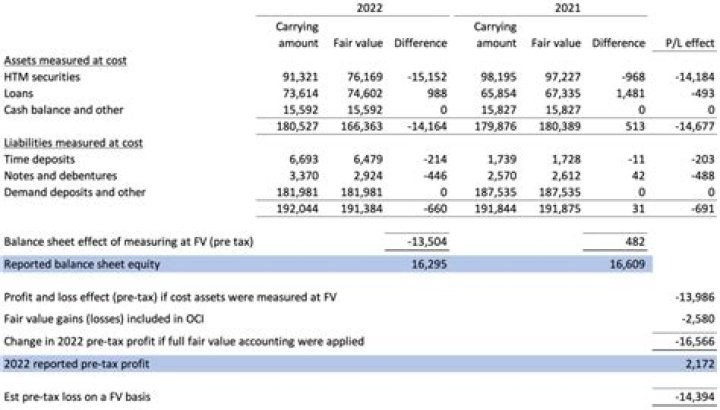

HTM securities are only reported as current assets if they have a maturity date of one year or less. Securities with maturities over one year are stated as long-term assets and appear on the balance sheet at the amortized cost—meaning the initial acquisition cost, plus any additional costs incurred to date.

How are available for sale securities reported?

Available-for-sale securities are reported at fair value. Unrealized gains and losses are included in accumulated other comprehensive income within the equity section of the balance sheet. Investments in debt or equity securities purchased must be classified as held to maturity, held for trading, or available for sale.

How are held to maturity securities valued?

Securities with maturities over one year are stated as long-term assets and appear on the balance sheet at the amortized cost—meaning the initial acquisition cost, plus any additional costs incurred to date. Both available for sale and held-for-trading securities appear as fair value on accounting statements.

Where is held to maturity securities on balance sheet?

Debt held to maturity is shown on the balance sheet at the amortized acquisition cost. To find the amortized acquisition cost the securities are amortized like a mortgage or a bond. Amortization Schedule: Debt held to maturity is shown on the balance sheet at the amortized acquisition cost.

Which of the following is the best definition of current liability?

It must be payable in cash. Which of the following is the best definition of a current liability? An obligation payable within one year or within the normal operating cycle, whichever is longer.

When stock is issued in exchange for property the best evidence of fair value might be any of the following except?

When stock is issued in exchange for property, the best evidence of fair value might be any of the following except: The average book value of outstanding stock. Red Inc. issues shares of stock with a par amount of $1 per share in exchange for a machine.

Can I buy stock and sell it the next day?

Retail investors cannot buy and sell a stock on the same day any more than four times in a five business day period. This is known as the pattern day trader rule. Investors can avoid this rule by buying at the end of the day and selling the next day.

Do Held to maturity securities affect net income?

Any earned income from held to maturity securities flows from the balance sheet to the income statement via the net investment income line item.

How do you account for AFS securities?

What is the difference between trading securities and available for sale securities?

Trading Securities—These securities are usually purchased with the intention to make profits in the short term. Available-for-Sale—These financial instruments are not actively managed with the intention to sell to make short-term profits. Instead, these securities are held and set by the companies at some point.

Why are held to maturity securities purchased?

Companies mostly use held to maturity securities to protect themselves against interest rate fluctuations, diversify their investment portfolios, and realize a small, low-risk capital gain over a longer period of time.

How do you record held to maturity securities?

Debt held to maturity is classified as a long-term investment and it is recorded at the market value (original cost) on the date of acquisition. All changes in market value are ignored for debt held to maturity. Debt held to maturity is shown on the balance sheet at the amortized acquisition cost.

When more than one security is sold for a single price?

When more than one security is sold for a single price and the total selling price is not equal to the sum of the market prices, the cash received is allocated between the securities based on: Relative market values.