When does the IRS send you a levy notice?

Mia Ramsey

Published Mar 01, 2026

Levy is the technical term for the IRS seizing your assets. Unlike other creditors, the IRS does not have to go to court to do this. They simply have to follow their own internal procedures with including sending you a notice.

When does an employer receive a wage Levy?

Thus, the levy process up to the issuance of a wage levy is entirely between the IRS and the taxpayer and does not involve the employer. If an employer receives a wage levy it usually means that the employee has either exhausted his rights or failed to exercise them in a timely manner.

How are wage levies figured on a tax return?

Information About Wage Levies. If you do not return the statement in three days, your exempt amount is figured as if you are married filing separately with no dependents (zero). If you have other income sources, the IRS may allocate the exemptions to the other income source and levy on 100% of the income from a particular employer.

Can a employer refuse to accept a wage Levy?

In certain cases, the IRS will notify the employer not to allow a certain deduction, such as a 401 (k) contribution, in which case the employer should follow the IRS’s instructions. Employers cannot accept a revised W-4 from an employee following receipt of a wage levy.

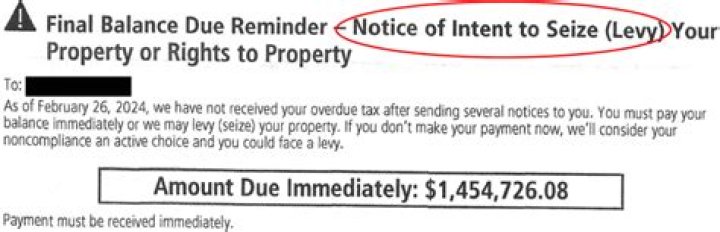

What happens if I ignore a notice of intent to levy?

If it is passed the deadline to appeal those changes, you may still be able to request an audit reconsideration or file an amended return. You still need to respond to the notice of intent to levy to try to get the IRS to give you time to resolve this dispute. What Happens if I Ignore a Notice of Intent to Levy?

What does a cp523 notice of intent to levy do?

The main purpose of a CP523 notice is to tell you the IRS intends to terminate your installment agreement. However, it also serves as a notice of intent to levy. How Should I Respond to a Notice of Intent to Levy?

How does levy on wages and other income work?

Continuous Effect of Levy on Salary and Wages Unlike other levies, a levy on a taxpayer’s wages and salary has a continuous effect. When other income is levied, the levy reaches a payment the taxpayer has a fixed and determinable right to.