When do I get Form 1099-C from my lender?

Andrew Mclaughlin

Published Feb 25, 2026

If you borrowed money from a commercial lender and at least $600 of that debt was canceled or forgiven, you should receive Form 1099-C from the lender (the IRS also receives a copy).

Can a 1099-C prove that a debt was canceled?

Bank argues that the 1099-C does not cancel the debt or prove that it canceled the debt. Bank argues that it stopped collection activity and issued the 1099-C simply to comply with IRS regulations. Bank argues that the 1099-C form alone is not sufficient to prove that it canceled the debt.

Why did the bank issue a 1099-C?

Bank asserts that it issued the 1099-C to comply with Internal Revenue Service regulations. The purpose of forms 1099-C are to show canceled or discharged debt as income to the borrower. When Debtors filed a subsequent tax return, they included the $59,667.34 of canceled debt from Bank as income and paid taxes on it.

What happens to your taxes when you get a 1099-C?

1 If a lender cancels or forgives a debt of $600 or more, it must send Form 1099-C to the IRS and the borrower. 2 If you receive a 1099-C, you may have to report the amount shown as taxable income on your income tax return. 3 Because it’s considered income, the canceled debt has tax consequences and may lower any tax refund you were due.

Do you have to pay taxes on a 1099-C debt?

In cases where the 1099-C canceled debt falls under an IRS exclusion—which means you don’t have to pay taxes on all or some of the income—you still may need to file a form. The creditor that sent you the 1099-C also sent a copy to the IRS. If you don’t acknowledge the form and income on your own tax filing, it could raise a red flag.

The Reeds argue that the Bank had thrown in the towel when it issued the 1099-C. The Bank, relying on the IRS guidance, argued that the 1099-C was not an admission that the debt was no longer due, but rather an effort to be in compliance with reporting regulations.

When do you need a 1099 for debt forgiveness?

Form 1099-C is a tax form required by the IRS in certain situations where your debts have been forgiven or canceled. The IRS requires a 1099-C form for certain acts of debt forgiveness because it considers that forgiven debt as a form of income. Did you find out about the negative item on your credit report?

What does Form 1099-C cancellation of debt mean?

What Is Form 1099-C: Cancellation of Debt? Form 1099-C (entitled Cancellation of Debt) is one of a series of “1099” forms used by the Internal Revenue Service (IRS) to report various payments and transactions, excluding employee wages.

Where to find fair market value on 1099-C?

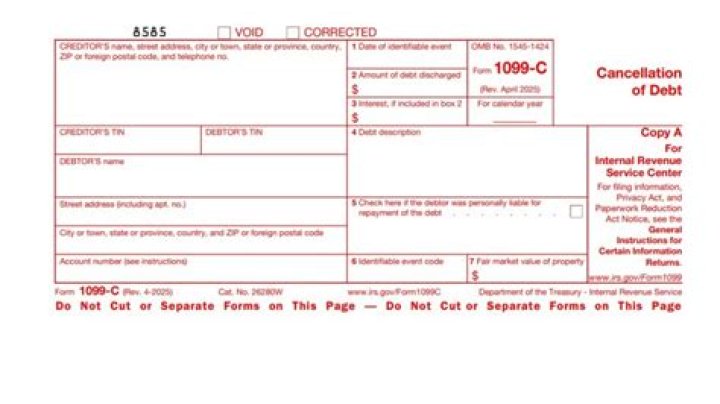

Box 7: Fair market value of property. If a foreclosure or abandonment of property occurred during the same year—and in connection with the canceled debt—box 7 shows the fair market value, or you will receive a separate 1099-A form. 4 1099C. All prior versions of Form 1099-C are available on the IRS website. 5

Is the forgiven debt on a 1099-C considered ordinary income?

This means that the amount forgiven that is included on your 1099-C form, will not be treated as ordinary taxable income to you on your tax return. This provision applies to debt forgiven in calendar years 2007 through 2017.

Where does canceled debt go on a 1099-C?

In most cases canceled debt counts as income. If you receive Form 1099-C, you must report the amount on your income tax return on the “Other income” line of your Form 1040 or 1040-SR. Note that you must include the canceled debt in your income even if it’s less than $600 and you don’t receive Form 1099-C. 2

Where do I report my 1099 income on my tax return?

If you receive Form 1099-C, you must report the amount on your income tax return on the “Other income” line of your Form 1040 or 1040-SR.

What do you have to report on Form 1099-C?

The only forgiven debt that must be reported on Form 1099-C is the debt principal then owed. This is consistent with the IRS explanation to borrowers quoted above where the IRS says “ [w]hen you borrow money, you don’t include the loan proceeds in gross income because you have an obligation to repay . . ..”

Why did I get a 1099-C bankruptcy form?

At its most basic level, a 1099-C reports a debt that was canceled, forgiven, never paid back or wiped out in bankruptcy. Here are some reasons you may have gotten a form 1099-C: You cut a deal with your credit card issuer and it agreed to accept less than you owed. You had a student loan or part of a student loan forgiven.

What does the right side of Form 1099-C show?

The right side of the form has seven boxes: Box 1: Date of identifiable event. Box 1 shows the date the earliest identifiable event occurred or the date of when the debt was discharged. Box 2: Amount of debt discharged.

When to file a claim on a timeshare?

You can file a claim on Form 1040X if the statute of limitations for filing a claim is still open. The statute of limitations generally does not end until 3 years after the due date of your original return. If the timeshare is resold it seems to not be material to their claim they forgave your obligation to them for the debt.

What happens when a debt is cancelled by a timeshare?

That’s not true. The 1099-C reporting of a cancelled debt is a tax obligation and does not invalidate the original underlying debt. The debt can most certainly be sold to another party and the debt buyer may attempt collection and even sue you unless suit is prohibited by the statute of limitations or time-barred.