When do estates and trusts have to file Form 1041?

Henry Morales

Published Feb 09, 2026

IRS Form 1041 can either be filed either according to the calendar year or a fiscal year. For calendar year estates and trusts, the Form 1041 must be filed by April 15 of the following year.

What are the instructions for Form 1041 for 2020?

Capital gain or loss from partnerships, S corporations, or other estates or trusts. A capital loss carryover from 2019 to 2020. For more information, see Pub. 544, Sales and Other Dispositions of Assets; Pub. 551, Basis of Assets; and the Instructions for Form 8949.

When do I need to file Form 1041 for Empowerment Zone?

The election to roll over gain from the sale of an empowerment zone asset is available for 2018 through 2020. If you are eligible for this benefit for tax years 2018 or 2019, you will need to file an amended Form 1041 return to claim it.

What are the steps in Schedule D Form 1041?

Lines 1 through 3. Line 4. Step 1. Step 2. Step 3. Line 10. Line 12. Installment sales. Step 1. Step 2. Step 3. Other sales or dispositions of section 1250 property. Section references are to the Internal Revenue Code unless otherwise noted. Section references are to the Internal Revenue Code unless otherwise noted.

What do you need to know about 1041 tax return?

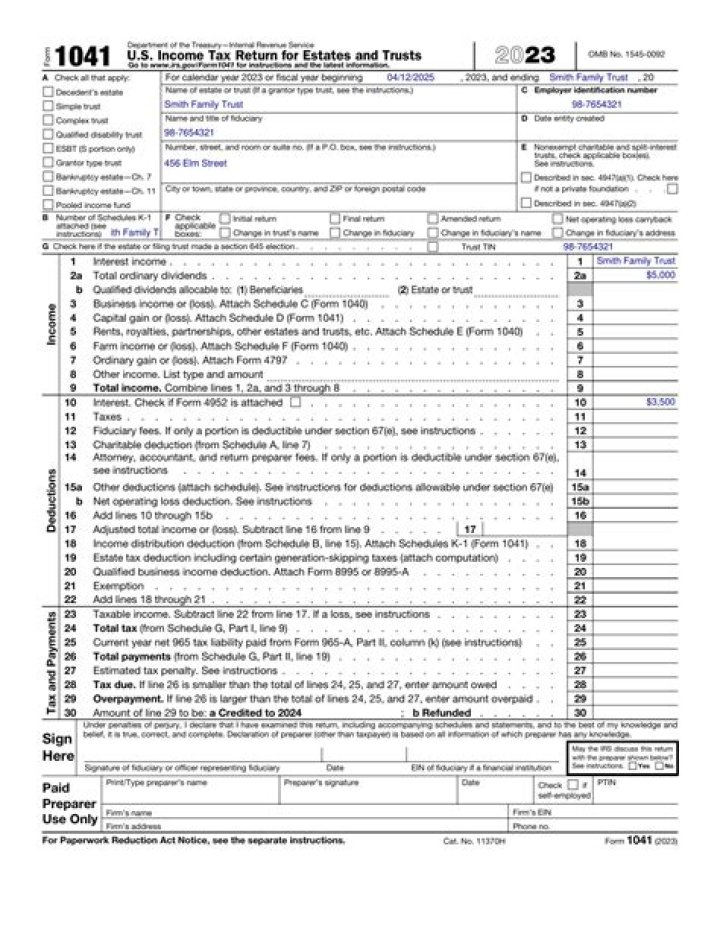

About Form 1041, U.S. Income Tax Return for Estates and Trusts. The fiduciary of a domestic decedent’s estate, trust, or bankruptcy estate files Form 1041 to report: The income, deductions, gains, losses, etc. of the estate or trust.

When to file Form 1041 and Schedule K-1?

For calendar year estates and trusts, file Form 1041 and Schedule (s) K-1 on or before April 15 of the following year. For fiscal year estates and trusts, file Form 1041 by the 15th day of the 4th month following the close of the tax year.

When do estates and trusts do not need to file tax returns?

For Estates With No Income. If the estate or trust has no income, or a gross income of less than $600 within the tax year, then there is no need to file a return. However, if one of the beneficiaries is a nonresident alien, then a trust or estate must file a tax return (even if it does not have any income). Deductions for Estates and Trusts

What do you need to know about Form 1041?

The fiduciary of a domestic decedent’s estate, trust, or bankruptcy estate files Form 1041 to report: The income, deductions, gains, losses, etc. of the estate or trust. The income that is either accumulated or held for future distribution or distributed currently to the beneficiaries. Any income tax liability of the estate or trust.

When to report excess deductions on Form 1041?

Schedule K-1 (Form 1041) Instructions—Corrected Decedent’s Schedule K-1– 29-JAN-2021 Reporting Excess Deductions on Termination of an Estate or Trust on Forms 1040, 1040-SR, and 1040-NR for Tax Year 2018 and Tax Year 2019 —

Can a trust or decedent claim an income tax deduction?

However, there is one major distinction. A trust or decedent’s estate is allowed an income distribution deduction for distributions to beneficiaries. Income distributions are reported to beneficiaries and the IRS on Schedules K-1 (Form 1041).