When borrowing costs are Capitalised?

James Williams

Published Feb 17, 2026

Borrowing costs are capitalised as part of the cost of a qualifying asset when it is probable that they will result in future economic benefits to the enterprise and the costs can be measured reliably. Other borrowing costs are recognised as an expense in the period in which they are incurred.

What does borrowing cost include MCQ?

Borrowing costs include interest on bank overdrafts and borrowings, finance charges on finance leases and exchange differences on foreign currency borrowings where they are regarded as an adjustment to interest costs.

When capitalization of borrowing cost should be started for a qualifying asset?

The capitalisation starts when all three conditions are met: expenditures are incurred, borrowing costs are incurred, and the activities necessary to prepare the asset for its intended use or sale are in progress. Expenditures on the asset are incurred when the prepayments are made (payments of the instalments).

What are the examples of qualifying asset?

Examples of qualifying assets are office buildings, hospitals, infrastructure assets such as roads, bridges and power generation facilities, and inventories that require a substantial period of time to bring them to a condition ready for use or sale.

What is the purpose of borrowing cost?

Borrowing costs are interest and other costs that an entity incurs in connection with the borrowing of funds. IAS 23 provides guidance on how to measure borrowing costs, particularly when the costs of acquisition, construction or production are funded by an entity’s general borrowings.

Which is required for borrowing cost incurred directly attributable to a qualifying asset?

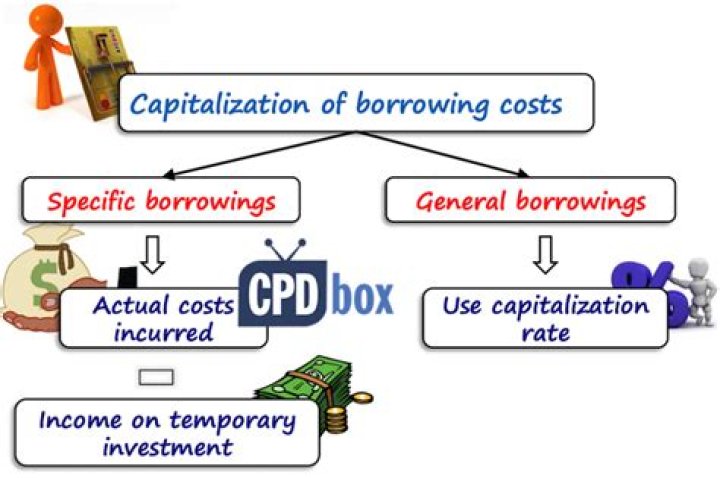

If the borrowing is directly attributable to a qualifying asset, the borrowing cost is required to be capitalized as cost of the asset. The amount of capitalized interest on general borrowing is the lower of actual interest incurred or computed capitalized interest.

Can borrowing costs be written off?

borrowing expenses on any portion of the loan you use for private purposes (for example, money you use to buy a car). If the total borrowing expenses are $100 or less, you can claim a full deduction in the income year they are incurred.

Which is not qualifying asset?

Other investments, and those assets that are routinely produced over a short period of time, are not qualifying assets. Assets that are ready for their intended use or sale when acquired also are not qualifying assets. they are incurred.

What is the cost of borrowing money on an annual basis?

Debt

| Question | Answer |

|---|---|

| Cost of borrowing money on an annual basis; takes into account the interest rate and other related fees on a loan | annual percentage rate (APR) |

| A decrease or loss in value | depreciation |

| A yearly fee that’s charged by the credit card company for the convenience of the credit card | annual fee |