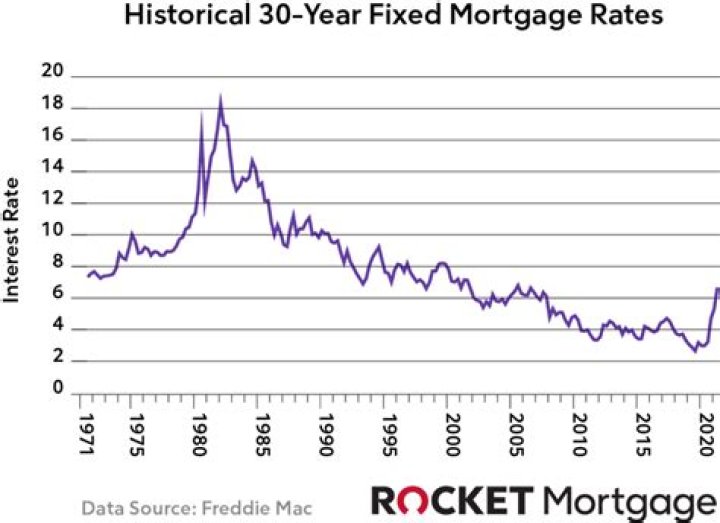

What were mortgage interest rates in 2014?

Andrew Mclaughlin

Published Mar 03, 2026

Rates went up to 4.17% in 2014.

Does Wells Fargo do interest rate modifications?

If you can’t afford your current mortgage due to a financial hardship, and you want to stay in your home, we may be able to change certain terms of the loan — such as the interest rate or the time allowed for repayment — to make your payments more affordable. There are multiple loan modification programs available.

What was the 15-year mortgage rate in 2014?

15-year mortgage rates vs. 30-year mortgage rates

| Year | 30-Year Mortgage Rate | 15-Year Mortgage Rate |

|---|---|---|

| 2012 | 2.93% | 3.66% |

| 2013 | 3.11% | 3.98% |

| 2014 | 3.29% | 4.17% |

| 2015 | 3.09% | 3.85% |

What has lower interest rate 15 or 30-year mortgage?

A 15-year mortgage costs less in the long run since the total interest payments are less than a 30-year mortgage. The cost of a mortgage is calculated based on an annual interest rate, and since you’re borrowing the money for half as long, the total interest paid will likely be half of what you’d pay over 30 years.

What’s the current interest rate on a Wells Fargo mortgage?

Wells Fargo home mortgage loans. Use our online tools to find your home price range, loan options, Today’s Mortgage Rates. Rates, terms, and fees as of 12/17/2020 10:15 AM Eastern Standard Time and subject to change without notice. 30-year Fixed Rate. Interest Rate 2.5%. APR

What kind of mortgage does Wells Fargo offer?

As far as Wells Fargo goes, the rates for fixed-rate jumbo mortgages aren’t necessarily that different from conventional mortgage rates, though you’ll likely need a much more substantial down payment.

How much down payment do you need for Wells Fargo mortgage?

However, you will need to have prepared some sort of down payment on the home and mortgage, a number that Wells Fargo seems to prefer around 25% of the value of the home, which is slightly higher than the typical 20% most lenders adhere to.

How can I lower my mortgage interest rate?

One last trick some folks use to reduce their mortgage interest expense is opening a second mortgage to pay off the first. It’s basically a form of arbitrage where rates are lower on the second than the first for one reason or another. This can be done with either a fixed-rate home equity loan or adjustable-rate HELOC.