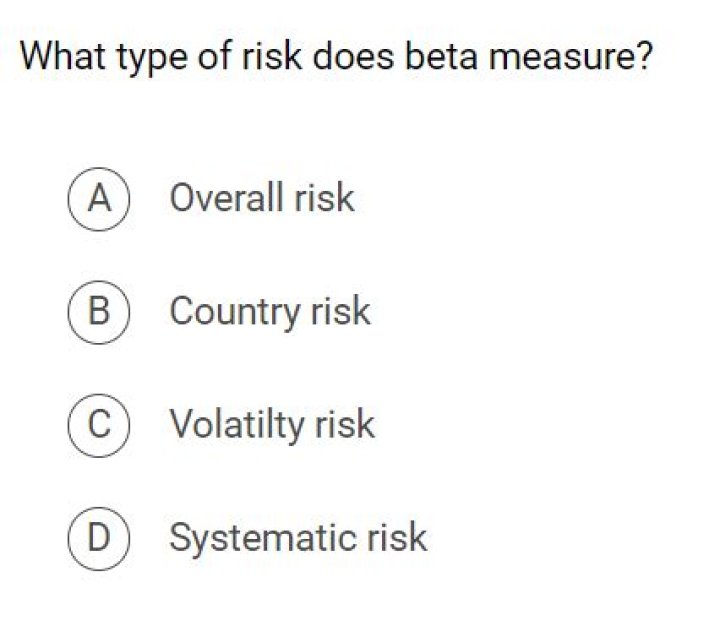

What type of risk does beta measure?

James Craig

Published Feb 17, 2026

systematic risk

Beta is a measure of the volatility—or systematic risk—of a security or portfolio compared to the market as a whole. Beta is used in the capital asset pricing model (CAPM), which describes the relationship between systematic risk and expected return for assets (usually stocks).

How is beta used in risk analysis?

Beta measures a stock’s volatility, the degree to which its price fluctuates in relation to the overall stock market. In other words, it gives a sense of the stock’s risk compared to that of the greater market’s. Beta is used also to compare a stock’s market risk to that of other stocks.

Why is beta an appropriate measure of risk?

Beta is a measure of a stock’s volatility in relation to the overall market. If a stock moves less than the market, the stock’s beta is less than 1.0. High-beta stocks are supposed to be riskier but provide higher return potential; low-beta stocks pose less risk but also lower returns.

Is beta a reliable measure of risk?

Risk, together with the willingness to accept it, are two key elements in determining the likelihood of stock market profitability. Beta, which is an analytical technique long used by security analysts and portfolio managers, is one of the best-known methods of measuring such risk.

What does a negative beta coefficient mean?

In regression analysis, the beta coefficient represents the change in the outcome variable for a unit change in the independent or predictor variable. A negative beta coefficient indicates the decrease in the dependent variable for a unit change in the independent variable.

How do you interpret a negative beta coefficient?

If the beta coefficient is negative, the interpretation is that for every 1-unit increase in the predictor variable, the outcome variable will decrease by the beta coefficient value.

What is a high negative beta?

In general, high beta means high risk, but also offers the possibility of high returns if the stock turns out to be a good investment. A negative beta coefficient, on the other hand, means the investment moves opposite of market direction.

How do you interpret beta weight?

A beta weight will equal the correlation coefficient when there is a single predictor variable. β can be larger than +1 or smaller than -1 if there are multiple predictor variables and multicollinearity is present. If the independent/dependent variables are not standardized, they are called B weights.