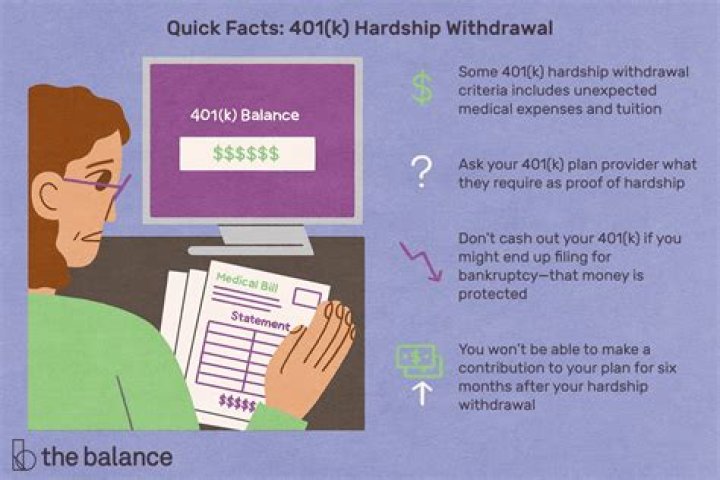

What qualifies as a hardship withdrawal for 401k cares act?

John Thompson

Published Mar 22, 2026

The CARES Act eliminates the 10% withdrawal penalty for qualified retirement account holders who have a valid Covid-19-related financial hardship. It allows them to withdraw up to $100,000 from their tax-deferred retirement accounts, or taxable earnings in a Roth account, in 2020.

Does 401k hardship withdrawal count as income?

Withdrawals from 401(k)s are considered income and are generally subject to income tax because contributions and growth were tax-deferred, rather than tax-free. If you have questions, check with a tax expert or financial advisor.

What are the rules for hardship withdrawal from a 401k?

If your plan allows for early distribution, the 401(k) hardship withdrawal rules for 2021 are as follows: You can only withdraw what you need. If you’re seeking money to fix your house after a flood and receive an estimate for $10,000, that is how much you’ll be approved to borrow.

Can a hardship distribution be made in a retirement plan?

Generally, a retirement plan can distribute benefits only when certain events occur. Your summary plan description should clearly state when a distribution can be made. The plan document and summary description must also state whether the plan allows hardship distributions, early withdrawals or loans from your plan account.

Do you have to pay taxes on a hardship withdrawal?

But you must pay taxes on the amount of the withdrawal. A hardship withdrawal can give you retirement funds penalty-free, but only for certain specific qualified expenses such as crippling medical bills or the presence of a disability.

When to take money out of a 401k?

Many 401(k) plans allow you to withdraw money before you actually retire for certain events that cause you a financial hardship. Many 401(k) plans allow you to withdraw money before you actually retire to pay for certain events that cause you a financial hardship.