What is traditional overhead allocation?

Andrew Ramirez

Published Feb 19, 2026

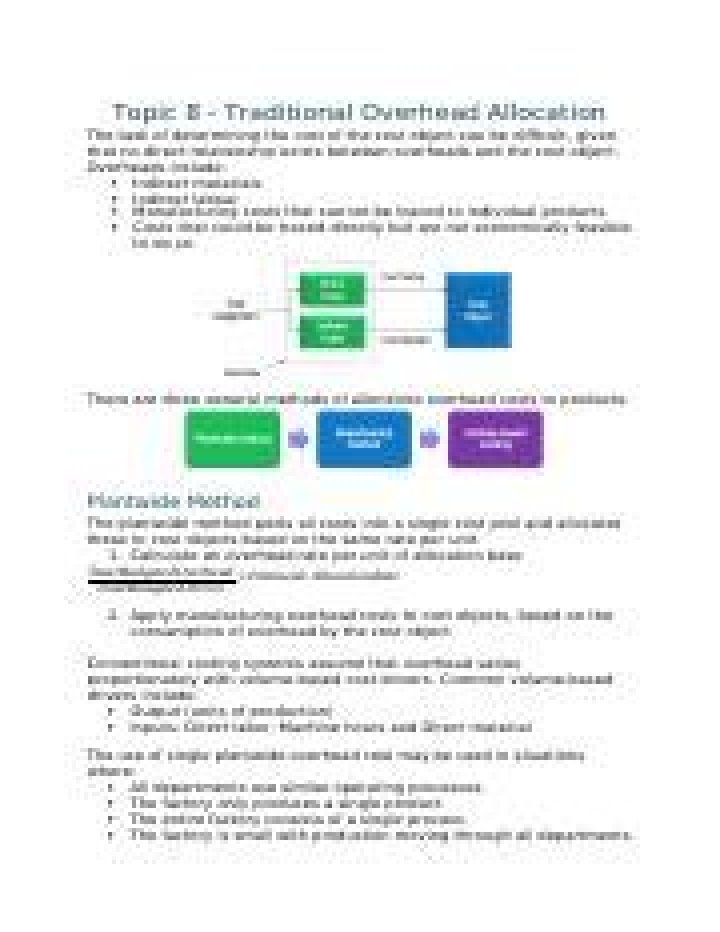

Traditional allocation involves the allocation of factory overhead to products based on the volume of production resources consumed, such as the amount of direct labor hours consumed, direct labor cost, or machine hours used. Direct labor is the work used in manufacturing that can be directly traced to the product.

What is the main problem with traditional cost accumulation systems?

The trouble with traditional costing is that factory overhead may be much higher than the basis of allocation, so that a small change in the volume of resources consumed triggers a massive change in the amount of overhead applied.

What is generally true about overhead allocation to high volume products versus low volume products under a traditional costing system?

4. What is generally true about overhead allocation to high-volume products versus low-volume products under a traditional costing system? Under a traditional costing system the overhead allocation will be high to high- volume products than the low volume products.

Why are direct labor hours and machine hours commonly used as the bases for overhead allocation?

The more direct labor hours worked, the higher the overhead costs incurred. Thus direct labor hours or direct labor costs would be used as the allocation base. If a company’s production process is highly mechanized (i.e., it relies on machinery more than on labor), overhead costs are likely driven by machine hours.

What is the reason for pooling costs quizlet?

What is the reason for pooling costs? Determining a pool rate for all costs incurred by the same activity reduces the number of cost assignments required.

What are the advantage and disadvantage in using the traditional way of accounting?

While a traditional accounting system is less expensive as far as up-front cost is concerned, in the long run, an automated accounting system is much less expensive and time-consuming while at the same time being much safer to store critical business data.

What is traditional cost allocation method?

Traditional allocation involves the allocation of factory overhead to products based on the volume of production resources consumed, such as the amount of direct labor hours consumed, direct labor cost, or machine hours used.

What will a company using traditional volume based overhead allocation cost methods tend to do when product diversity exists?

Product Diversity As the Cooper Pen Company example illustrates, when production volume diversity exists, using a production volume based allocation method tends to cause high volume products to be charged with too much overhead and low volume products to be charged with too little overhead.

Is activity-based costing better than traditional?

Activity-Based Costing Benefits Activity based costing systems are more accurate than traditional costing systems. This is because they provide a more precise breakdown of indirect costs. However, ABC systems are more complex and more costly to implement.

What is the traditional method of allocating overhead?

In other words, the traditional method implies there is only one driver of the factory overhead and the driver is machine hours (or direct labor hours, or some other indicator of volume produced). In reality there are many drivers of the factory overhead: machine setups, unique inspections, special handling, special storage, and so on.

Why are overhead allocations overstated in activity based costing?

A company that uses a traditional two stage cost allocation approach is likely to do the following. a. Overhead allocations to high volume products will tend to be overstated while overhead allocations to low volume products will tend to be understated. 9.

What happens if the allocation of manufacturing overhead is wrong?

The message here is this: Even if each product’s costs are wrong due to inaccurate allocations of manufacturing overhead, it is still possible that the financial statements will be accurate and receive a clean audit report.

What is the weakness of traditional cost allocations?

What is the weakness of traditional cost allocations? Traditional cost allocations are often based on volume such as number of products manufactured, number of direct labor hours, number of production machine hours, number of square feet, etc.