What is the time limit for issuing debit note?

James Craig

Published Apr 17, 2026

In such cases, where the value of supply declared in the original invoice is lower as compared to the revised amount, a debit note is issued to give effect to the increase in prices. Further, the law does not provide any time limit to issue debit notes.

How long do you have to dispute an invoice UK?

If you’re not happy with our response to your query, you can dispute it. You must do this in writing within 21 days of hearing back from us about your query.

How late can an invoice be issued and remain valid UK?

6 years

What is the legal time limit for invoices in the UK? Old or unpaid invoices remain valid for up to 6 years in the UK. Based on the 1980 Limitations Act, invoices remain valid and must be settled within this time limit. An acknowledgement of the debt can extend this period.

Is there a time limit to bill for services rendered?

If a bill is legitimate, then they can bill you at any time for it, up to the statute of limitations in your particular state. There is no time limit. But best practice is to send bill to a customer ASAP.

Can debit note be issued after 6 months?

As per the provision of section 34(2) of CGST Act,2017 time limit to issue Credit note is as under: “A supplier can issue a credit note against a Tax Invoice on or before 30th September of the next financial year or the date of filing of annual return pertaining to the Tax Invoice, whichever is earlier.”

Can we issued credit note after 6 months?

Section 34(2) of the CGST act says that any registered dealer can issue a credit note in relation to supply of goods or services up to a period of six months from the end of the financial year or the date of filing the annual return, whichever is earlier.

How late can a company bill you?

There is no time limit. But best practice is to send bill to a customer ASAP. As soon as job is completed, goods delivered etc etc. The longer you wait – the longer the customer will wait to make the payment.

Can credit note be issued after 1 year?

What is the time limit for issuing tax invoice under GST?

In case of services, however, invoice has to be issued before or after provision of services. If the invoice is issued after provision of service, it has to be done within the specified period of 30 days from the date of supply of service, as per invoice rules.

What is the time limit for GST credit note?

The records of the credit have to be retained until the expiry of seventy-two months from the due date of furnishing of annual return for the year pertaining to such accounts and records.

How is the time limit for issue of invoice related to time of supply?

Who can issue an invoice within 45 days from the date of supply of service? If the supplier is a bank or a financial institution a GST invoice can be issued within 45 days from the date of supply of services.

What is the time limit allowed under the Income Tax Act?

The time limit to re-open income tax assessment cases has been reduced to 3 years from 6 years. Also, in case of serious tax evasion, the assessment can be reopened until 10 years, only when concealment of income is more than 50 lakh.

Can we issue credit note after one year?

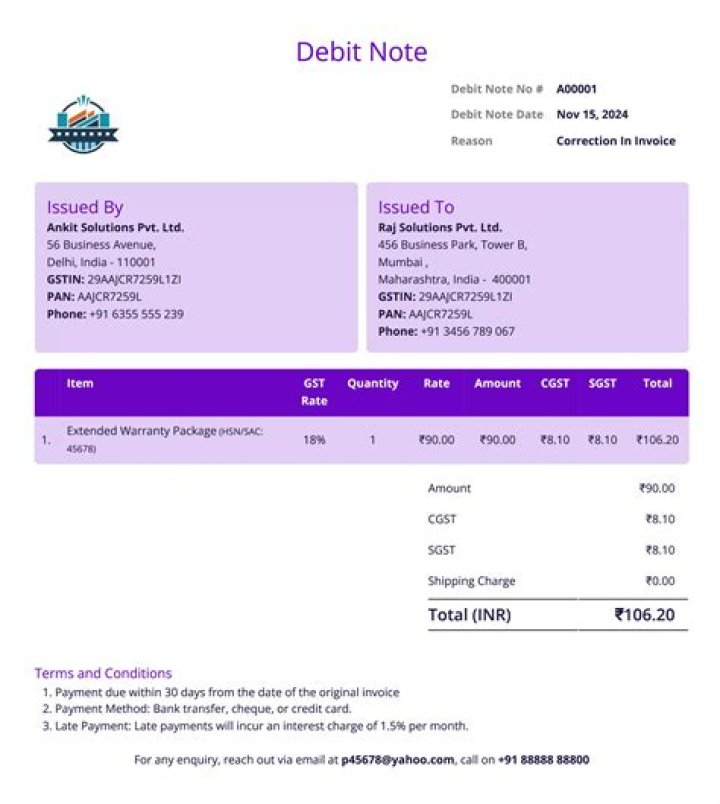

What is the time limit for debit note in GST?

seventy- two months

The records of the debit note or a supplementary invoice have to be retained until the expiry of seventy- two months from the due date of furnishing of annual return for the year pertaining to such accounts and records.

What is the time limit for GST registration?

within 30 days

The period for applying for GST registration is within 30 days of becoming liable to obtain GST registration. The individual shall obtain GST registration when the entity crosses the threshold aggregate turnover, initiates business involved in inter-state supplies or involved in e-commerce transactions.

What is current income in income tax?

Income Tax Slabs and Rates for Financial Year: 2019-20

| Income Tax Slab | Individuals below the age of 60 years |

|---|---|

| Up to `2,50,000 | Nil |

| 2,50,001 to 5,00,000 | 5% |

| 5,00,001 to 10,00,000 | 12,500 + 20% of total income exceeding 5,00,000 |

| Above 10,00,000 | 1,12,500 + 30% of total income exceeding 10,00,000 |