What is the split-off point of joint products?

Henry Morales

Published Feb 20, 2026

A split-off point is the location in a production process where jointly manufactured products are henceforth manufactured separately; thus, their costs can be identified individually after the split-off point. Prior to the split-off point, production costs are allocated to jointly manufactured products.

What are joint products joint costs and split-off point?

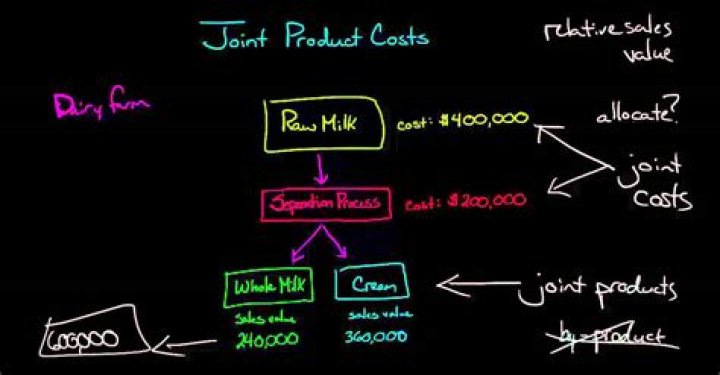

It may be defined as the cost incurred to produce two or more different products by processing one or more raw materials through a common production process or a series of production processes. The joint cost is incurred upto the split-off point (the point at which various products are separated).

How is split-off point calculated?

The split-off point is the point at which joint production stops and processing for separate products begins. Divide the sales value of each product by the total sales to determine the relative sales value of each product.

What is the split-off point and why is it important in analyzing joint costs?

The point at which the business can determine the final product is called the split-off point. There may even be several split-off points; at each one, another product can be clearly identified, and is physically split away from the production process, possibly to be further refined into a finished product.

What split off?

A split-off is a corporate reorganization method in which a parent company divests a business unit using specific structured terms. In a split-off, the parent company offers shareholders the option to keep their current shares or exchange them for shares of the divesting company.

Why are joint costs irrelevant in the sell or process further decision?

It is irrelevant for any sell-or-process-further decisions because the joint product cost are sunk cost. Similarly, what is sell or process further? The sell or process further decision is the choice of selling a product now or processing it further to earn additional revenue.

What is the difference between a spin off and a split-off?

A spin-off distributes shares of the new subsidiary to existing shareholders. A split-off offers shares in the new subsidiary to shareholders but they have to choose between the subsidiary and the parent company.

What is a tax-free split-off?

Basics of a Tax-Free Spin-Off A tax-free spinoff occurs when a corporation carves out and separates part of its business to form a new standalone entity, but the separation does not subject the parent firm to paying taxes.

How are allocated joint costs treated when making a sell or process further decision?

Joint costs are irrelevant to a sell-or-process-further decision because they are sunk costs and will not change whether the decision is to sell the existing product or process it further. Therefore, joint costs are ignored in this decision.

What is sales value at split off?

1. Sales-Value-at-Split-Off Method a. The sales-value-at-split-off method allocates joint cost based on each product’s proportionate share of market or sales value at the split-off point. b. In this method, the higher the market value, the greater the joint cost assigned to the product.

Which products should be sold at split-off and which products should be processed further?

Which product(s) should be sold at the split-off point? Answer: A product should be sold at the split-off point if there is not any incremental profit from processing the product further. As long as the process as a whole is profitable, it is irrelevant if an individual product is not profitable.

Are joint costs allocated to by products?

Joint Cost Allocation Allocate joint costs to the primary output products of the joint process, not the incidental byproducts or scrap. Allocate them using a physical measure or a monetary measure.

What is reversal cost method?

Reversal cost method is based on the theory that the cost of a by-product is related to its sales value. It is a step towards the recognition of a by-product cost prior its split off from the main product. It is also the nearest approach to methods employed in joint product costing.

What is split-off method?

A split-off is a corporate reorganization method in which a parent company divests a business unit using specific structured terms. There can be several methods for structuring a divestiture. Split-offs, spinoffs, and carveouts are a few options, each with its own structuring.

Why is cost allocation necessary in a joint process?

There are several important reasons why you spend time figuring and allocating joint costs: You need to calculate joint costs to calculate inventoriable costs. Those costs are attached to inventory and expensed when the product is sold. So you need joint costs to calculate inventory values and the cost of goods sold.

What are the 3 methods that joint costs can be allocated?

Three methods of allocating joint product costs are the physical units method, the market value method, and the net realizable method. The constant gross margin percentage method is also used to allocate joint cost.

How are process costs divided between joint products?

There are two main methods of apportioning the common process costs at the split-off point: • Physical measurement (weight or volume) of output. • Market value (sales or net realisable value) of output. The apportionment of common process costs between joint products is arbitrary whichever method is used.

When is a split off point in a production process?

June 30, 2018/. A split-off point is the location in a production process where jointly manufactured products are henceforth manufactured separately; thus, their costs can be identified individually after the split-off point.

How is market value calculated for joint products?

Market value is also a relatively straightforward method of common cost apportionment when the joint products can be sold at the split-off point. The output of each product is multiplied by their selling price at the split-off point to provide the respective weighting to be applied to the common costs.