What is the meaning of corridor amortization?

Andrew Mclaughlin

Published Feb 17, 2026

Corridor amortization occurs when the accumulated OCI (G/L) balance gets too large. The gain or loss is too large when it exceeds the arbitrarily selected FASB criterion of 10% of the larger of the beginning balances of the projected benefit obligation or the market-related value of the plan assets.

What is the corridor approach in accounting?

The corridor approach is a technique used to reduce the amounts of gains and losses to be recognized as an adjustment to pension expense. It requires recognition of certain gains and losses in excess of 10 percent of the greater of the projected benefit obligation or the market-related asset value.

How do you find the amortization of a corridor?

The procedure is as follows:

- Compare the PBO at the beginning of the year to the market value of the pension fund at that time and choose the larger figure.

- Take 10% of this figure. This is the corridor amount.

- Compare the unrecognized gain or loss at beginning of year to the corridor amount.

What is a corridor pension?

What Is the Corridor Rule? In pension accounting, the corridor rule requires the disclosure of any actuarial gain or loss that exceeds 10% of the greater of the pension benefit obligation or the market value of the plan’s assets and allows this actuarial gain or loss to be amortized over time into the income statement.

What is an actuarial gain?

Actuarial gain or loss refers to an increase or a decrease in the projections used to value a corporation’s defined benefit pension plan obligations.

How should Gains or losses related to pension plan assets be recognized?

How should gains or losses related to pension plan assets be recognized? How does this treatment compare to that for gains or losses related to the pension obligation? Gains or losses related to pension plan assets represent the difference between the return on investments and what the return had expected to be.

How is pension asset/liability calculated?

In most cases, the plan obligation is larger than the plan assets, thus creating the liability. The quick and easy calculation for pension liability is found using this formula: Pension assets minus pension obligations equals pension liability.

Is Amortization a gain or loss?

As a minimum, amortization of a net gain or loss included in accumulated [OCI] (excluding asset gains and losses not yet reflected in market-related value) shall be included as a component of net pension cost for a year if, as of the beginning of the year, that net gain or loss exceeds 10 percent of the greater of the …

What is amortization of prior service cost?

Definition. The term amortization of prior service cost refers to the systematic recognition of a pension expense in future periods resulting from a retroactive change to the plan’s benefit formula.

Is amortization a gain or loss?

How do you calculate pension expenses?

Pension Expense = increase in the DBO/PBO during the accounting period. Current Service Cost = amount by which a company’s defined benefit obligation increases as a result of employee service during the accounting period.

What is the treatment of actuarial gains or losses?

Actuarial gains and losses comprise the difference between the pension payments actually made by an employer and the expected amount. A gain occurs if the amount paid is less than expected. A loss occurs if the amount paid is higher than expected.

Are actuarial gains distributable?

Actuarial gains and losses are recognised immediately in the statement of total recognised gains and losses. They are not recycled into the profit and loss account in subsequent periods.

Are pension assets on balance sheet?

The pension asset on the balance sheet is the fair value of the pool of assets at the balance sheet date. Actual return on assets: These pension assets are a pool of investments, held for the long-term benefit of the employees, and their value moves with the market.

Is PBO an asset or liability?

A corporation reports a pension asset on its balance sheet when the fair value of its plan assets is higher than the present value of its pension benefits, the projected benefit obligation (PBO). It reports a pension liability when the PBO is higher than the fair value of plan assets.

Are plan assets on the balance sheet?

Plan assets are presented in the balance sheet at their fair value where they are netted off against plan liabilities to determine the pension asset/liability. …

What are amortization expenses?

Amortization expenses account for the cost of long-term assets (like computers and vehicles) over the lifetime of their use. Also called depreciation expenses, they appear on a company’s income statement. This continues until the cost of the asset is fully expensed or the asset is sold or replaced.

How is prior service cost amortized quizlet?

Prior service cost is amortized on a years-of-service method or on a straight-line basis over the average remaining service life of active employees.

How do you calculate amortization corridor?

Gains or losses related to the pension obligation are treated the same way. However, firms report the net difference between those two amounts, referred to as the “funded status” of the plan, as either a net pension liability (if underfunded) or a net pension asset (if overfunded).

How do you amortize prior service costs?

Prior service costs should be amortized by assigning an equal amount to each future period of service of each employee active at the date of the amendment who is expected to receive benefits under the plan.

What is the corridor rule in financial accounting?

In financial accounting, the corridor rule is a materiality rule that requires disclosure of a pension actuarial gain or loss, if the gain or loss exceeds 10% of the greater of the Pension Benefit Obligation (PBO) or the fair value of plan assets. If this is the case, then the corridor rule allows this actuarial gain…

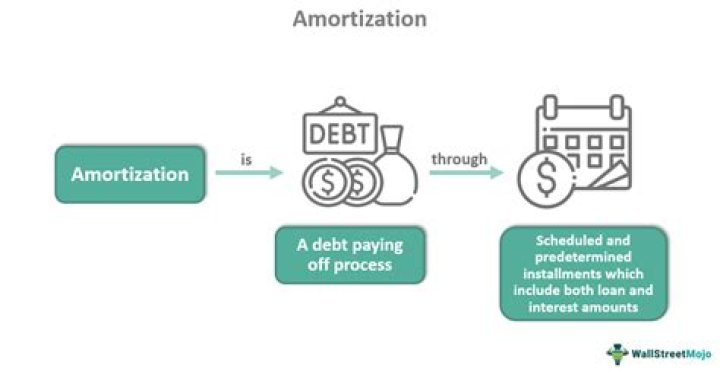

What is amortization and how is it used in accounting?

Amortization is an accounting technique used to periodically lower the book value of a loan or intangible asset over a set period of time. The term “amortization” can refer to two situations. First, amortization is used in the process of paying off debt through regular principal and interest payments over time.

What is the difference between amortization and impairment?

Impairment occurs when an intangible asset is deemed less valuable than is stated on the balance sheet after amortization. Amortization and impairment both relate to the value of a company’s intangible assets, which are reported on the balance sheet.

When does amortization of intangible assets take place?

Updated Jun 25, 2019. Amortization is an accounting technique used to periodically lower the book value of a loan or intangible asset over a set period of time. The term “amortization” can refer to two situations. First, amortization is used in the process of paying off debt through regular principal and interest payments over time.