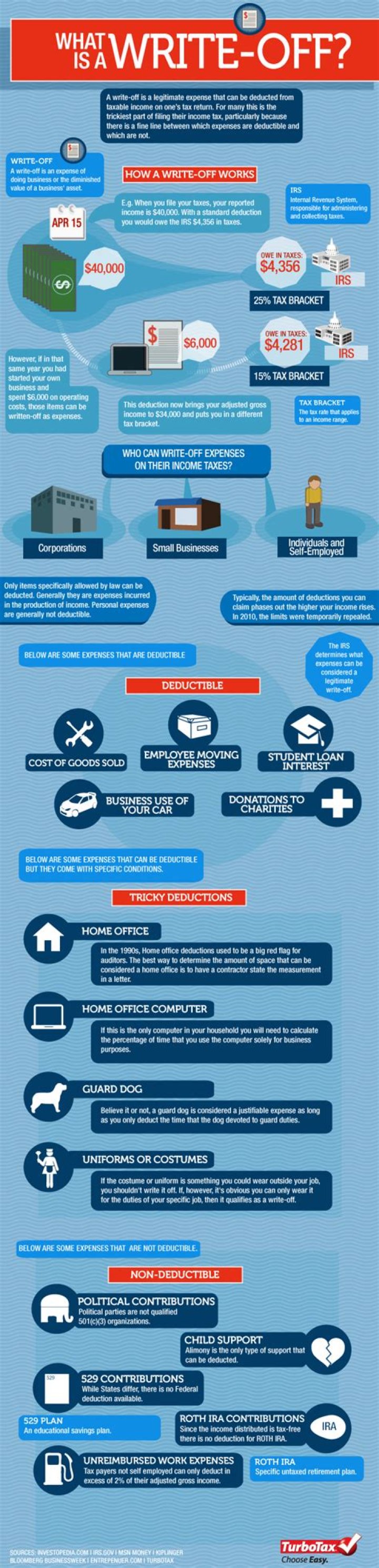

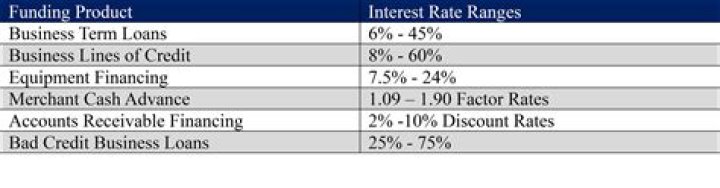

What is the interest rate for a business loan?

Emma Jordan

Published Feb 19, 2026

Average business loan interest rate by loan type

| Loan type | Annual interest rate (AIR) |

|---|---|

| Traditional bank loan | 2% to 13% |

| SBA loan | 3.75% to 10.25% |

| Online loan | 7% to 100% |

| Merchant cash advance | 20% to 250% |

What’s the payment on a $500 000 mortgage?

Monthly payments on a $500,000 mortgage At a 4% fixed interest rate, your monthly mortgage payment on a 30-year mortgage might total $2,387.08 a month, while a 15-year might cost $3,698.44 a month.

How much do I need to earn to borrow 500k?

Gill McLean: An applicant who is single, with no debts and no dependent children would need to earn approximately $87,000 per annum to qualify for a loan of this amount. The deposit required on a loan amount of $500,000 would be approximately $52,000 if a client were purchasing a property to the value of $530,000.

How much deposit do I need for a business loan?

Most lenders need 10 – 30% of the loan value as a deposit. This money can come from savings, working capital, alternative finance instruments or as an external investment. The deposit amount you’ll need for your business loan depends on various factors: These include: The amount of money borrowed.

How much can I borrow with 50k deposit?

If you’ve been able to save a large deposit to buy a home, a lender will likely lend you more. However, lenders will generally not let you borrow more than 90% of a property’s value. For example, if a property costs $500,000 and you have a $50,000 the deposit, the lender will only lend you $450,000.

Can you borrow 100 for a business loan?

You may be able to get a 100% commercial loan with a combination of equity in an existing residential property that you own, a guarantor or your own business assets, including client book and equipment.

Can I borrow more if I have a large deposit?

So the rule of thumb for most providers is that the larger your deposit, the cheaper your mortgage rate will be. This is because a larger deposit will pay off a larger chunk of the property value, meaning that you’ll most likely borrow less and the lower the loan-to-value.