What is the IFRS requirement for contingent liabilities?

Sarah Duran

Published Feb 16, 2026

An entity recognises a provision if it is probable that an outflow of cash or other economic resources will be required to settle the provision. If an outflow is not probable, the item is treated as a contingent liability.

Can you Capitalise restructuring costs?

If the costs cannot be immediately deducted, they generally are required to be capitalized as an asset, although these capitalized costs often can be deducted over some period of time. Costs associated with a restructuring generally can only be immediately deducted if the proposed transaction is not completed.

How do you account for restructuring costs?

Restructuring costs are reported as non-operating charges and aren’t expected to recur in the future. Although they are non-recurring costs, they still are reported in the income statement and used to calculate the net income.

What qualifies as restructuring?

IAS 37 defines a restructuring as a program that materially changes the scope of a business or the manner in which it is conducted. Understanding the scale of the restructuring is therefore important because not all programs may qualify for cost recognition under IFRS.

What are restructuring liabilities?

Restructuring Liabilities means all unpaid costs and expenses (including Other Taxes and severance but excluding Income Taxes) of the Company or its Subsidiaries related to or arising out of the Commercial Restructuring.

Are restructuring charges non cash?

Non-cash charges can also reflect one-time accounting losses that are driven by changing balance sheet items. Such charges are often the result of changes to accounting policy, corporate restructuring, the changing market value of assets or updated assumptions on realizable future cash flows.

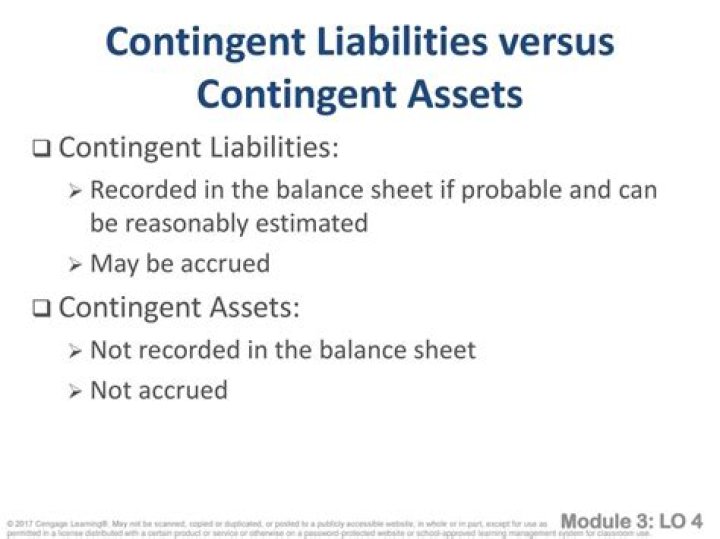

Why contingent liabilities are not shown in the balance sheet?

Contingent liabilities, liabilities that depend on the outcome of an uncertain event, must pass two thresholds before they can be reported in financial statements. If the contingent loss is remote, meaning it has less than a 50% chance of occurring, the liability should not be reflected on the balance sheet.

What is a restructuring expense?

Restructuring expense is defined as the cost a company incurs during corporate restructuring. They are considered nonrecurring operating expenses and, if a company is undergoing restructuring, they show up as a line item on the income statement.

A contingent liability is (IAS 37.10; 27-30): a possible obligation that arises from past events and whose existence will be confirmed only by the occurrence or non-occurrence of one or more uncertain future events not wholly within the control of the entity; or.

Is restructuring provision a liability?

Restructurings are often triggered by mergers and acquisitions. Under IFRS 33 , the cost of restructuring an acquiree is recognized as a liability as part of the acquisition accounting – i.e. as a debit to goodwill rather than expensed – only if it is an obligation of the acquiree at the date of acquisition.

When does restructuring become a liability under IFRS 33?

When is IFRS 3 recognition of restructurings or exit activities?

IFRS 3 Recognition of restructurings or exit activities – Liabilities related to restructurings or exit activities of the acquiree should only be recognized at the acquisition date if they are preexisting liabilities of the acquiree and were not incurred for the benefit of the acquirer.

Can you include incremental costs in IFRS restructuring?

Only incremental costs that are directly associated with the restructuring should be included in the provision. Additionally, IFRS prohibits the recognition of a provision for costs associated with ongoing activities, such as the cost of training or relocating continuing staff.

Why are contingent liabilities not recognised in IFRS?

Contingent liabilities also include obligations that are not recognised because their amount cannot be measured reliably or because settlement is not probable. Contingent liabilities do not include provisions for which it is certain that the entity has a present obligation that is more likely than not to lead to an outflow …