What is the distinguishing factor between fraud and error?

James Craig

Published Mar 13, 2026

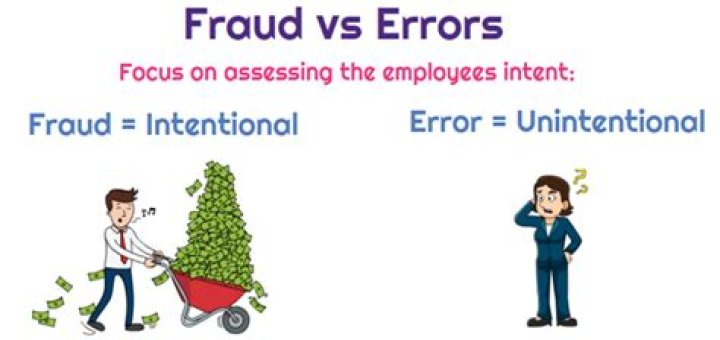

02 Misstatements in the financial statements can arise from either fraud or error. The distinguishing factor between fraud and error is whether the un- derlying action that results in the misstatement of the financial statements is intentional or unintentional.

What are the different types of errors and frauds?

Types of Errors: Clerical Errors: Such an error arises on account of wrong posting. Errors of Commission : When amount of transaction or entry is incorrectly recorded in accounting books/ledger. Errors of Omission : When the transactions are not recorded in the books of original entry or posted to the ledger.

What is the difference between fraud and irregularities?

As nouns the difference between irregularity and fraud is that irregularity is (countable) an instance of being irregular while fraud is any act of deception carried out for the purpose of unfair, undeserved and/or unlawful gain.

What are the differences between errors frauds and illegal acts?

Errors are unintentional, they are mistakes. Fraud has intent. Fraud is defined as “wrongful or criminal deception intended to result in financial or personal gain”. Illegal acts are violations of laws, regulations, bribery.

What is needed to protect an organization from fraud?

An excellent way to prevent fraud in any organization is to have an open-door policy because it encourages open communication between employees and the management. Furthermore, the policies and procedures of the company should be unbiased and fair.

Which of the following is an example of how a fraud perpetrator would rationalize his actions?

white-collar criminals. Which of the following is an example of how a fraud perpetrator would rationalize his actions? computer fraud.

What are the reasons and circumstances of errors?

Accounting errors can take place either intentionally or innocently. The main causes of accounting errors are as follows: 1. Lack of Accounting Knowledge: The books of accounts are maintained following certain accounting principles, due to lack of accounting principles and rules, accounting error may occur.

What is management’s responsibility regarding fraud?

Management’s responsibilities include creating an environment where fraud is not tolerated, identifying risks of fraud, and taking appropriate actions to ensure that controls are in place to prevent and detect fraud.

How can you protect from fraud?

8 Ways to Protect Yourself from Fraud

- Guard your online information.

- Monitor your accounts.

- Business Email Compromise.

- Shred sensitive documents.

- Check your credit report.

- Think twice about sharing your information.

- Filter your phone calls.

- Report suspicious activity.

What are the three main components of the fraud triangle?

Essentially, the three elements of the Fraud Triangle are: Opportunity, Pressure (also known as incentive or motivation) and Rationalization (sometimes called justification or attitude). For fraud to occur, all three elements must be present.

What are the three ways auditors respond to fraud risks?

What are 3 ways auditors respond to fraud risks? the risk of management override of controls. contra accounts. fixed assets to increase earnings.

What are sources of error?

Common sources of error include instrumental, environmental, procedural, and human. All of these errors can be either random or systematic depending on how they affect the results. Instrumental error happens when the instruments being used are inaccurate, such as a balance that does not work (SF Fig. 1.4).

What are compensating errors with examples?

For example, the wages expense could be too high by $2,000 due to one error, while the cost of goods sold could be too low by $2,000 due to a compensating error. Or, the revenue account balance could be too low by $5,000, but it is offset by a compensating error in the same amount in the utilities expense account.

Who is responsible for detection of fraud?

Who is responsible for preventing and detecting fraud? According to the auditing standards, the primary responsibility for the prevention and detection of fraud rests with the governing body and management.

What are the auditor’s responsibilities to detect fraud?

Auditor’s Responsibilities Discussions with management and others within the company relating to fraud. Identifying and assessing fraud risks. Responding to fraud risks (including determining or altering the nature, timing, and extent of audit procedures to be performed) The evaluation of audit evidence.

How can you protect yourself from financial fraud?

Tips to Protect Yourself from Financial Fraud

- Don’t put your personal information online.

- Shred your trash.

- Check your credit report frequently.

- Put spending alerts on your credit cards.

- Check your bills.

- Think twice before sharing private information of any kind.

- Don’t click on links online.

Do all credit cards have fraud protection?

All credit cards provide protection against fraud, and by law you’re not liable for more than $50 of fraudulent charges (assuming you catch the fraud and report it). Reputable financial companies won’t call you unsolicited, and you’re already plenty protected by your credit card company, anyway.

What is the most important element of the fraud triangle?

Fraud triangle has three elements – Pressure, opportunity, and rationalization, and the most crucial factor is an opportunity. It is so because the opportunities available for committing the fraud give motivation to the fraudsters to commit the fraud.