What is the difference between secured and unsecured debt?

Ava Robinson

Published Feb 19, 2026

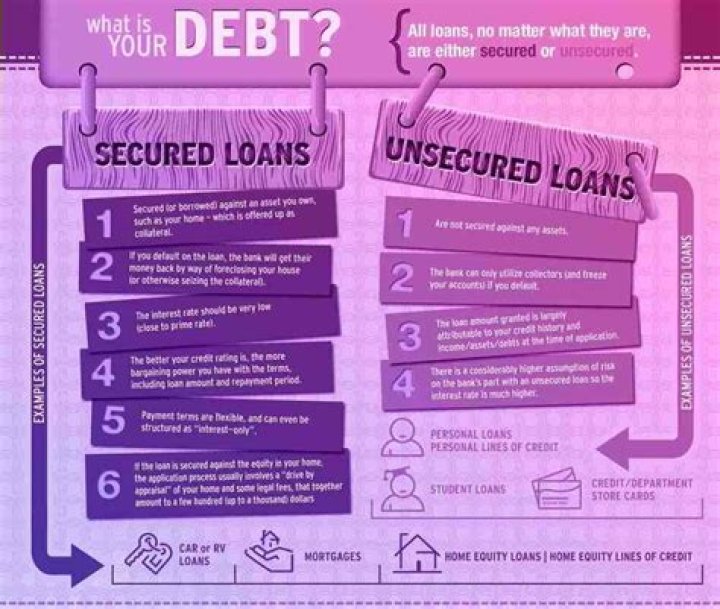

While secured debt uses property as collateral to support the loan, unsecured debt has no collateral attached to it. However, because of collateral connected to secured debt, the interest rates tend to be lower, loan limits higher and repayment terms longer.

Which of the following best describes the difference between secured and unsecured debt?

Which describes the difference between secured and unsecured credit? Secured credit is backed by an asset equal to the value of a loan, while unsecured credit is not guaranteed by a material object.

What is an unsecured debt security?

An unsecured debt is a debt for which the creditor does not have a security interest in collateral, and the creditor is therefore not entitled to take property from you to satisfy that debt without a judgment. Common types of unsecured debt are credit cards, medical bills, most personal loans, and student loans*.

What are secured and unsecured loans explain by giving examples?

A secured loan is one that is connected to a piece of collateral – something valuable like a car or a home. A car loan and mortgage are the most common types of secured loan. An unsecured loan is not protected by any collateral. If you default on the loan, the lender can’t automatically take your property.

How can unsecured debt be reduced?

To get rid of unsecured debt with creditors who do not allow snowflake payments or that charge a fee to process these payments, consider consolidating these debts with a different lender. You can also try to negotiate with creditors to reduce interest rates or modify payment plans to help get rid of debt more quickly.

What are unsecured loans examples?

An unsecured loan is a facility to acquire loans using one’s outstanding credit score, without pledging any collateral like a house or car. Personal loans, credit cards, student loans are some examples of uncollateralized loans.

How long does an unsecured debt last?

Under the Limitation Act 1980 a creditor has six years to chase most unsecured unpaid debts, or twelve years for some mortgage shortfalls. This ‘limitation period’ starts from the time of your last payment or acknowledgement of the debt, not the total length of time you’ve been making payments.

What are the main advantages of a secured and unsecured loan quizlet?

What are the main advantages of a secured and unsecured loan? Secured: requires collateral which the lender can take but offers lower interest rates. Unsecured; does not require collateral but is more risky and therefore comes with higher rates.

How do you tell if your loan is secured or unsecured?

Basically, a secured loan requires borrowers to offer collateral, while an unsecured loan does not.

What happens when you can’t pay back an unsecured loan?

Although not paying these loans may not result in immediate forfeiture of collateral, as it would with a secured arrangement, leaving an unsecured debt unpaid can lead to collection attempts, damaged credit ratings and, in extreme cases, lawsuits.

What to do if you can’t pay back an unsecured loan?

Whatever your security is, the lender has the right to sell it to reclaim their money if you don’t repay the loan as agreed. There’s no security on an unsecured loan. But the lender on an unsecured loan can still add extra charges and report your missed payments to credit reference agencies.

What happens if you stop paying unsecured debt?

What Happens if I Default on an Unsecured Loan? Just because an unsecured loan is not secured does not mean there are no consequences if you fail to repay the debt or fail to make your payments on time. Most creditors assess hefty late payment fees each month that your payment is not received on time.

What are the main advantages of a secured vs unsecured loan?

Disadvantages

| Secured Loans | Unsecured Loans | |

|---|---|---|

| Advantages | • Lower interest rates • Higher borrowing limits • Easier to qualify | • No risk of losing collateral • Less risky for borrower |

| Disadvantages | • Risk losing collateral • More risky for borrower | • Higher interest rates • Lower borrowing limits • Harder to qualify |

Unsecured debt has no collateral backing. Lenders issue funds in an unsecured loan based solely on the borrower’s creditworthiness and promise to repay. Secured debts are those for which the borrower puts up some asset as surety or collateral for the loan.

What is an example of an unsecured debt?

Common types of unsecured debt are credit cards, medical bills, most personal loans, and student loans*. These debts help you do something (buy items, pay your doctor, get an education), but they are not backed by a specific asset. To compel payment, the creditor has to sue you and get a judgment against you.

Why is collateral important?

Before a lender issues you a loan, it wants to know that you have the ability to repay it. That’s why many of them require some form of security. This security is called collateral which minimizes the risk for lenders. It helps to ensure that the borrower keeps up with their financial obligation.

Can a unsecured loan be written off?

Is it Possible to Write Off Unsecured Debt? The simple answer to this is ‘yes’. The first thing you can try to do is ask your creditor to write off your debts using our free letter template.

Do I have to pay back unsecured debt?

What happens if you default on an unsecured loan? An unsecured personal loan is a loan that you borrow from a bank or private lender. You agree to make regular repayments calculated based on the interest rate charged – until you’ve paid it off completely. As these are unsecured loans, no asset is tied to it.

How do I know if my loan is secured or unsecured?

Why do banks demand collateral while issuing a loan?

if the borrower is not able to make payment of the loan on time then the lender has right to sale the collateral and recover the money. so whenever any bank or any lender gives loan to anyone they demand collateral so that they can feel assured about the recovery of loan amount.

How is a secured debt different from an unsecured debt?

A secured debt is connected to specific property, which is put up as collateral to secure the loan. Common secured debts are mortgages backed by real estate and car loans secured by the motor vehicle. An unsecured debt is not connected to any specific piece of property, such as credit card debts and medical bills.

Can a property serve as collateral for a secured debt?

Almost without exception, if you’re making payments on an item of property, you’ve agreed that the property will serve as collateral for repayment of the debt.

Can a secured debt be discharged in bankruptcy?

You have personal liability for a secured debt just as you would for any other debt. You’re obligated to pay the debt to the creditor. Chapter 7 bankruptcy wipes out this personal liability if it’s the type of debt that can be discharged in bankruptcy.

Can a creditor Sue you for a secured debt?

Once your personal liability is eliminated, the creditor cannot sue you to collect the debt. Security interest. The second part of a secured debt is the creditor’s legal claim (lien or security interest) on the property that serves as collateral for the debt.