What is the difference between FIFO method and weighted average method while calculating equivalent units?

Andrew Mclaughlin

Published Feb 17, 2026

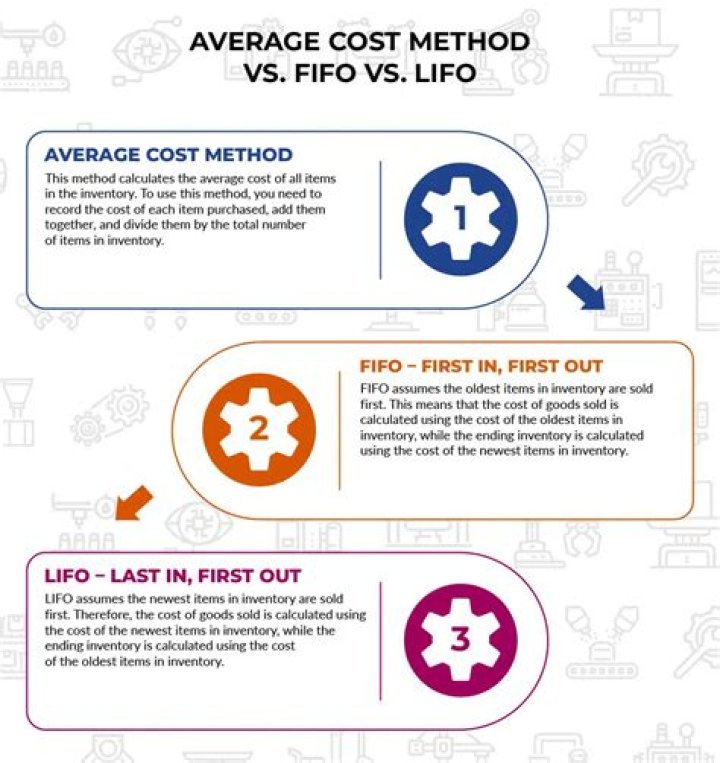

According to the Accounting for Management website, the main difference between the FIFO and weighted average method is in the treatment of beginning work-in-process or unfinished goods inventory. The weighted average method includes this inventory in computing process costs, while the FIFO method keeps it separate.

How are the equivalent units for the beginning work in process treated under the FIFO method of process costing?

Remember, under FIFO, these are finished first so their costs must be passed along to completed units. Costs to complete beginning work in process: you will take the Equivalent units calculated for completing beginning work in process x the cost per equivalent unit.

How do you calculate EUP using FIFO?

FIFO Costing EUP Calculation for Direct Materials Under FIFO costing, beginning WIP units for EUP are calculated by multiplying beginning WIP units by the percentage remaining to be completed at the beginning of the period because the percentage completed was included in the prior period calculation.

Why should the FIFO method be called a modified or department FIFO method?

FIFO should be called a modified or departmental FIFO method because the goods transferred in during a given period usually bear a single average unit cost (rather than a distinct FIFO cost for each unit transferred in) as a matter of convenience.

How do you calculate units transferred out?

Total costs assigned to units transferred out equals the cost per equivalent unit times the number of equivalent units. For example, costs assigned for direct materials of $96,000 = 60,000 equivalents units (from step 1) × $1.60 per equivalent unit (from step 3).

What is a major advantage of using the FIFO method for purposes of planning and control?

A major advantage of FIFO is that managers can judge the performance in the current period independently from the performance in the preceding period.

What is concept of FIFO method?

First In, First Out, commonly known as FIFO, is an asset-management and valuation method in which assets produced or acquired first are sold, used, or disposed of first. For tax purposes, FIFO assumes that assets with the oldest costs are included in the income statement’s cost of goods sold (COGS).