What is the difference between book income and taxable income?

John Thompson

Published Feb 19, 2026

Book income describes a company’s financial income before taxes. It is the amount a corporation reports to its investors or shareholders and gives an idea of how well a company performed during a certain period of time. Tax income, on the other hand, is the amount of taxable income a company reports on its return.

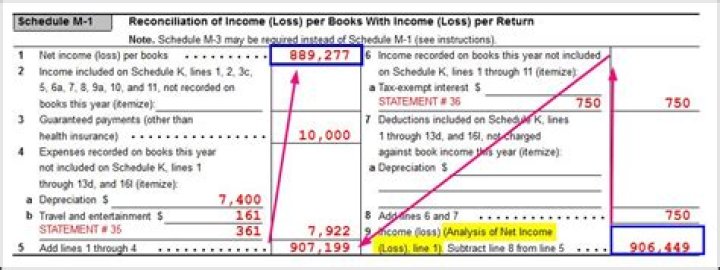

What are book to tax differences?

Here is a list of the common book-to-tax differences we see so that you can understand the differences between your book and taxable income.

- Depreciation and amortization.

- Allowance for doubtful accounts.

- Inventory reserves for slow-moving, excess or obsolete inventory.

- Accrued accounts.

- Travel and entertainment.

What is book income tax?

Book income is the amount of income corporations publicly report on their financial statements to shareholders. This measure is useful for assessing the financial health of a business but often does not reflect economic reality and can result in a firm appearing profitable while paying little or no income tax.

What is difference between book and tax depreciation?

Generally, the difference between book depreciation and tax depreciation involves the “timing” of when the cost of an asset will appear as depreciation expense on a company’s financial statements versus the depreciation expense on the company’s income tax return.

What meals are subject to the 50 deduction limit?

Meal expense that are 50% deductible:

- Meals directly related to business meetings of employees, stockholders, agents, and directors.

- Office meetings and partner meetings.

- Meals with clients, customers, and vendors that will benefit the business.

- Meals while on business travel status.

Do you pay tax on depreciation?

Depreciation divides the cost associated with the use of an asset over a number of years. Since depreciation of an asset can be used to deduct ordinary income, any gain from the disposal of the asset must be reported and taxed as ordinary income, rather than the more favorable capital gains tax rate.

What are the two exceptions to the 50 rule?

EXCEPTIONS TO THE 50% LIMIT Food and Beverages for Employees – Expenses for food and beverages furnished on your business premises primarily for employees. For example, during group meetings, mentoring, on occasion if overtime work is required, during conferences, seminars or training schools.