What is taxable temporary difference?

Sarah Duran

Published Feb 15, 2026

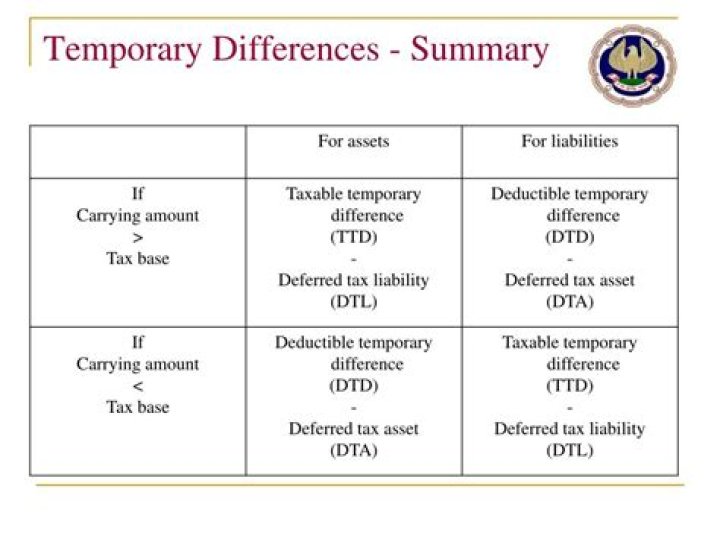

A temporary difference is the difference between the carrying amount of an asset or liability in the balance sheet and its tax base. Taxable. A taxable temporary difference is a temporary difference that will yield taxable amounts in the future when determining taxable profit or loss.

What is the difference between a future taxable amount and a future deductible amount?

Future taxable amounts increase taxable income and result in deferred tax liabilities for financial reporting purposes; future deductible amounts decrease taxable income and result in deferred tax assets for financial reporting purposes.

When accounting for income tax is a temporary difference?

A temporary difference, however, creates a more complex effect on a company’s accounting. If a temporary difference causes pre-tax book income to be higher than actual taxable income, then a deferred tax liability is created.

Is Depreciation a permanent or temporary difference?

The company is reporting an expense on the current tax return but reports it for financial statement purposes in the future. Depreciation is a great example of this. Quite a few accounting events lead to a temporary difference for book versus tax.

What is a future deductible amount?

The second type of temporary difference is a future deductible amount. The company is reporting an expense on the current tax return but reports it for financial statement purposes in the future. Depreciation is a great example of this.

What percent is tax on purchases?

7.25%

Local Rates

| State | State Tax Rate | Combined Rate |

|---|---|---|

| Arkansas | 6.50% | 9.47% |

| California (b) | 7.25% | 8.66% |

| Colorado | 2.90% | 7.65% |

| Connecticut | 6.35% | 6.35% |

Taxable temporary differences are those on which tax will be charged in the future when the asset (or liability) is recovered (or settled).

Do temporary differences affect effective tax rate?

Often, the only impact is that the effective tax rate on the books will be higher or lower than the effective tax rate on the company’s tax return. If a temporary difference causes pre-tax book income to be higher than actual taxable income, then a deferred tax liability is created.

How do you calculate future taxable amount?

The nominal amount of the future income taxes is equal to the differences multiplied by the applicable tax rate. Using generally accepted accounting principals (GAAP) requires that, when reported to financial statements, income earned matches to expenses incurred during the same period.

What items of temporary difference result in future taxable amounts and what items will result in future deductible amounts?

A temporary difference that will result in future deductible amounts and, therefore, will usually give rise to deferred income tax asset. Costs of guarantees and warranties are estimated and accrued for financial reporting purposes.

Is a tax credit a permanent difference?

Since they are not reversed, permanent differences do not give rise to deferred tax assets or liabilities. Examples of the items which give rise to permanent differences include: Tax credits for some expenditures directly reduce taxes. …

Is depreciation a permanent or temporary difference?

Depreciation. Most accounting books emphasize this example of a temporary difference: For book purposes, the company may use straight-line depreciation, whereas for tax purposes, it may use a more accelerated method, such as IRC Section 179.