What is systematic risk in stock market?

John Thompson

Published Feb 15, 2026

Systematic risk refers to the risk inherent to the entire market or market segment. Systematic risk, also known as “undiversifiable risk,” “volatility” or “market risk,” affects the overall market, not just a particular stock or industry.

Which stock has the highest systematic risk?

Stocks with a beta greater than 1.00 tend to rise and fall by a greater percentage than the market—that is, they have a high level of systematic risk and are very sensitive to market changes. Conversely, a stock with a beta less than 1.00 has a low level of systematic risk and is less sensitive to market swings.

How do you calculate systematic risk of a stock?

What is Systematic Risk?

- Er = Rf + β(Rm – Rf)

- Stockreturn = α + βRm + ε

- Correlationstock,market = βσm / σstock

What is the level of risk for stocks?

Your “Risk Level” is how much risk you are willing to accept to get a certain level of reward; riskier stocks are both the ones that can lose the most or gain the most over time.

What sign indicates systematic risk?

Since beta indicates the degree to which an asset’s return is correlated with broader market outcomes, it is simply an indicator of an asset’s vulnerability to systematic risk. Hence, the capital asset pricing model (CAPM) directly ties an asset’s equilibrium price to its exposure to systematic risk.

Can unsystematic risk be eliminated?

Unsystematic risk can be described as the uncertainty inherent in a company or industry investment. This risk is also known as a diversifiable risk since it can be eliminated by sufficiently diversifying a portfolio.

What is difference between systematic and unsystematic risk?

Unsystematic Risk in detail: Systematic risk is the probability of a loss associated with the entire market or the segment. Whereas, Unsystematic risk is associated with a specific industry, segment, or security.

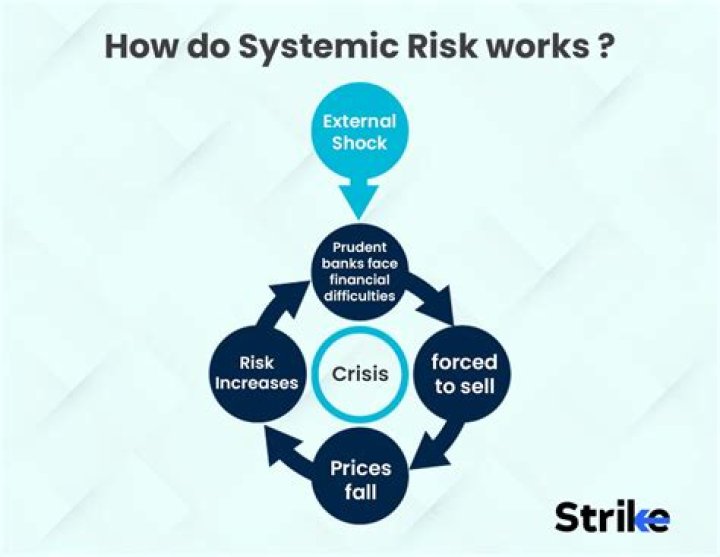

Is an example of systematic risk?

Examples of systematic risks include: Macroeconomic factors, such as inflation, interest rates, currency fluctuations. Environmental factors, such as climate change, natural disasters, resource, and biodiversity loss. Social factors, such as wars, changing consumer perspectives, population trends.

Can market risk be eliminated?

Market risk cannot be eliminated through diversification. Specific risk, or unsystematic risk, involves the performance of a particular security and can be mitigated through diversification. Market risk may arise due to changes to interest rates, exchange rates, geopolitical events, or recessions.

How can you prevent unsystematic risk?

The best way to reduce unsystematic risk is to diversify broadly. For example, an investor could invest in securities originating from a number of different industries, as well as by investing in government securities.