What is self-created intangible?

Andrew Ramirez

Published Apr 10, 2026

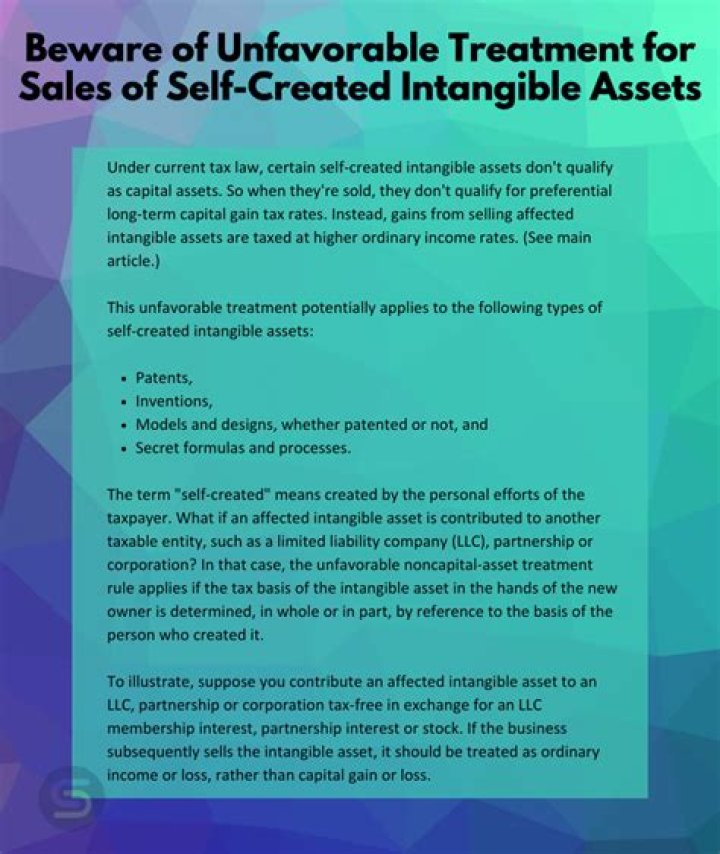

The change potentially applies to the following types of self-created intangible assets: Patents, Inventions, Models and designs (patented or not), and. Secret formulas and processes.

Is self-created goodwill a capital asset?

Self-created goodwill is a capital asset because the law doesn’t specifically exclude it from being a capital asset. Thus, your sale of self-created goodwill is a capital gain. Acquired goodwill is an amortizable Section 197 intangible. You recover its cost in equal monthly amounts over 15 years.

Is self-created goodwill a 1231 asset?

Acquired goodwill is an amortizable Section 197 intangible. When you sell the acquired goodwill, it’s a Section 1231 asset if you held it for more than one year, which means you qualify for the best of all tax worlds: If you have a net gain, it is a long-term capital gain.

Are self created intangibles amortizable?

Since many self-created and acquired intangible assets are amortizable under Code §167 and all Code §197 intangible assets are treated as subject to Code §167, Code §1245 will impact the characterization of gain on the sales of many types of intangible assets.

How are sales of intangible assets taxed?

Intangible assets or properties derive their value from intellectual content or other non-physical attributes. Typically, the sale or trade of a capital asset is taxed at the capital gain or loss tax rate. Conversely, the sale or trade of a non-capital asset is taxed at the ordinary gain or loss tax rate.

Is goodwill tax deductible in the US?

Tax information If you itemize deductions on your federal tax return, you may be entitled to claim a charitable deduction for your Goodwill donations. According to the Internal Revenue Service (IRS), a taxpayer can deduct the fair market value of clothing, household goods, used furniture, shoes, books and so forth.

Can you tax intangible assets?

While the IRS doesn’t tax intangible assets, it does tax income from them. That income is taxed by the Internal Revenue Service. On your financial accounting, you might assign a monetary value to intangibles, but in your tax accounting, you only count the income, not the value of the asset itself.