What is Section 481 A adjustment?

Emma Jordan

Published Feb 27, 2026

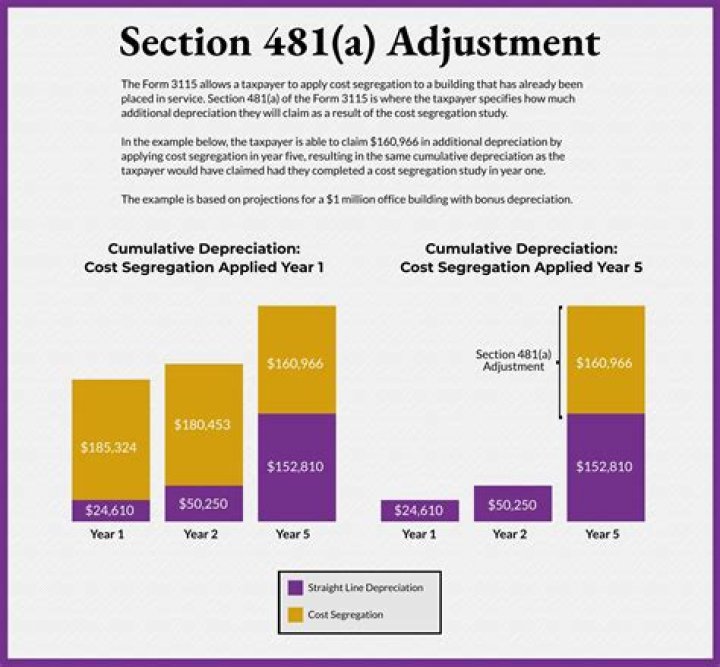

What is a 481(a) Adjustment? Under current IRS rules, the calculation of depreciation or repair deductions for prior years can be recomputed, and a one-time catch-up adjustment (i.e. IRC §481(a) adjustment) is allowed in the current tax year for missed deductions.

What is an Internal Revenue Code Section?

The Internal Revenue Code (IRC) refers to Title 26 of the U.S. Code, the official “consolidation and codification of the general and permanent laws of the United States,” as the Code’s preface explains.

What title is the Internal Revenue Code?

Title 26

The Internal Revenue Code (IRC) is the body of law that codifies all federal tax laws, including income, estate, gift, excise, alcohol, tobacco, and employment taxes.

How is a property divided by the Internal Revenue Code?

Property is divided into certain sections within the Internal Revenue Code (IRC) that determine everything from how the property is treated at sale, to how the property is depreciated, to the nature and character of the gain on sale of the asset.

How are tax returns and tax return information confidential?

Generally, tax returns and tax return information are confidential, as required by 26 U.S.C. 6103. Background Section 460, which was enacted by section 804 of the Tax Reform Act of 1986, Public Law 99-514 (100 Stat. 2085, 2358-2361), generally requires a taxpayer to determine the taxable income from a long-term contract using the percentage-of-

What is the IRS transaction code for TC 016?

TC 016 with special DLN xx96388888888X is generated to validate sole proprietor SSN in the entity. Updates no other entry data. May include other entity changes shown in TC 012, 013, 014, and 015. Doc Code 80/81 updates the EO Entity Section.

Who is the Associate Chief Counsel for the IRS?

Patrick Clinton of the Office of the Associate Chief Counsel (Income Tax and Accounting), (202) 317-7005 (not a toll-free number). This document contains final regulations under section 274 of the Code that amend the Income Tax Regulations ( 26 CFR part 1 ).