What is revenue basis accounting?

Sarah Duran

Published Feb 19, 2026

Under the accrual basis accounting, revenues and expenses are recognized as follows: Revenue is realized or realizable. Revenue is earned when products are delivered or services are provided. Realized means cash is received. Realizable means it is reasonable to expect that cash will be received in the future.

Which basis of accounting recognizes expenses?

Accrual accounting

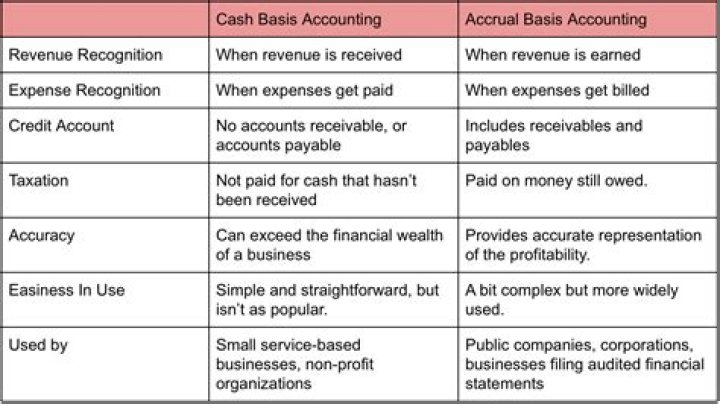

Accrual accounting is a method of accounting where revenues and expenses are recorded when they are earned, regardless of when the money is actually received or paid. For example, you would record revenue when a project is complete, rather than when you get paid. This method is more commonly used than the cash method.

What are the criteria accountants use to determine when to recognize revenue?

Before revenue is recognized, the following criteria must be met: persuasive evidence of an arrangement must exist; delivery must have occurred or services been rendered; the seller’s price to the buyer must be fixed or determinable; and collectability should be reasonably assured.

Is unearned revenue used in cash basis accounting?

Cash received before it is earned is considered unearned revenue. A cash accountant would debit cash and credit revenue as soon as the cash is received. An accrual accountant would debit cash and credit unearned revenue. Once the revenue has been earned, an accrual accountant debits unearned revenue and credit revenue.

Is cash basis or accrual basis better?

Cash basis accounting is easier, but accrual accounting portrays a more accurate portrait of a company’s health by including accounts payable and accounts receivable. The accrual method is the most commonly used method, especially by publicly-traded companies as it smooths out earnings over time.

Are there adjusting entries in cash basis accounting?

Companies using the cash basis do not have to prepare any adjusting entries unless they discover they have made a mistake in preparing an entry during the accounting period. Most companies use the accrual basis of accounting.

What is the formula of cash basis?

Under the cash-basis method, you may not record any expenses that you have been billed for but have not paid. Subtract your total cash-basis expenses from your cash-basis income. The result is your net income using the cash -basis accounting method.