What is refinance purchase?

Ava Robinson

Published Mar 24, 2026

Purchase mortgages, as the name implies, are mortgages used to finance the purchase of a home. Refinances, on the other hand, are used to “refinance” an existing mortgage. You can have a purchase mortgage without a refinance loan.

Can you refinance right after purchase?

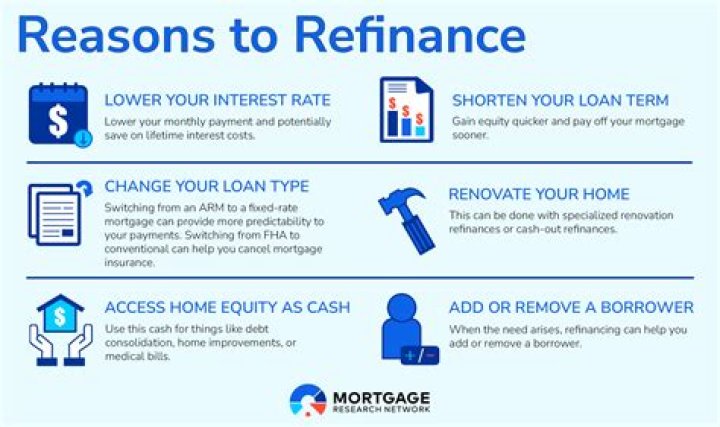

Lowering your monthly payments is always popular, especially with interest rates as low as they are now. However, most lenders won’t refinance a mortgage they issued in the last 120-180 days, so you may have to shop for a new lender. Switching loan types is helpful when your situation changes.

Are purchase and refi rates the same?

Historically, mortgage refinance rates are significantly higher than mortgage rates to purchase a home. But today’s refinance rates across all terms linger around the same level as purchase rates, representing a great bargain for homeowners looking to shorten their term and save big on interest.

How soon can I refi after purchase?

You can refinance your mortgage as many times as it makes financial sense to do so. The only caveat is that you might have to wait six months from your most recent closing (whether it was a purchase or previous refinance) to do it again. Also, remember that refinancing includes closing costs.

Why is refi rate higher than purchase?

Cash-out refinance: When a borrower requests a cash-out refinance, that means they want to change the loan rate and loan term of their mortgage while also taking money from the equity in their home. These borrowers are typically offered a higher APR than other borrowers because their default risk is greater.

Why refinance rate is lower than purchase?

The demand quickly became overwhelming for lenders to keep up with. At the same time, most borrowers get a lower interest rate when they refinance, meaning the lender earns less money over the life of the loan. And they seem to be willing to pay more than the amount new home buyers are paying for their mortgage loans.

Do you need an appraisal to refinance with the same lender?

Most lenders require that you get an appraisal or other form of home valuation before you refinance a mortgage. An appraisal assures the lender that they aren’t loaning you too much money for your property. You may not need an appraisal to refinance your loan if you have an FHA loan, VA loan or a USDA loan.

Are rates higher for refinance?

Refinance and purchase loans typically have the same rate. Borrowers might notice slightly higher refinance rates when they’re in demand.

Is it easier to refinance than purchase?

Refinancing borrowers have one other advantage. It is much easier for them than for borrowers purchasing a house to use a no-cost mortgage shopping strategy. Most of the settlement costs on a refinance are lender fees, and the third party services that generate charges (such as appraisal or credit) are often waived.

Purchase mortgages and refinances are both home loans, but they serve very different purposes. A purchase mortgage is a type of loan that homebuyers apply to finance the purchase of a new home. A refinance mortgage is the process homeowners go through to change their mortgage rate and terms.

Can you use a purchase appraisal for a refinance?

An appraisal could help you get approved for a refinance loan if you don’t qualify for the streamline programs. If your home is worth more than the market price and you owe less than 80%, you could eliminate the need for a private mortgage insurance policy, as well as reduce your mortgage rate.

Can I purchase and refinance at the same time?

When refinancing and buying at the same time isn’t a good idea. You shouldn’t refinance a home you intend to sell in the next six months or so because it’s not cost-efficient. This means you cannot refinance a primary residence, close on a second home, and then immediately move into it permanently.

Is it better to buy or refinance?

Homeowners who plan to remain in an existing home for several years or face financial strain are generally better off refinancing. On the other hand, homeowners who want a larger or smaller home, or one in a different location or with different features, should consider buying a new home only when they can afford it.

Can underwriter change appraised value?

The underwriter must review the appraisal and make a case to the FHA for why value is supported despite these factors. However, if the property doesn’t sell within a certain timeframe, the process changes to an appraisal-based claim, and the lender is only reimbursed at the new appraised value.

What do I need to refinance my investment property?

For example, candidates must have a great credit score and 6 months’ worth of assets to handle the mortgage on their rental and primary residences. Click here to check today’s investment property refinance rates. Applicants will also have to present tax information, rental lease agreements, and other property income information.

What are the requirements for a Freddie Mac refinance?

Freddie Mac Refinance Programs. Refinance Mortgages Topic “No Cash-out” Cash-out Special Purpose Cash-out Seasoning No requirement At least one Borrower must have been on title to the subject property for at least six months prior to the Note Date of the cash- out refinance Mortgage.

When is a rental property eligible for a cash out refinance?

There is an exception for properties that meet the Delayed Financing guidelines. Delayed Financing Rule: A rental property that was purchased within the last six months is eligible for a cash out refinance if: The new loan amount is no more than the original purchase price plus closing costs.