What is process cost flow?

Andrew Ramirez

Published Feb 14, 2026

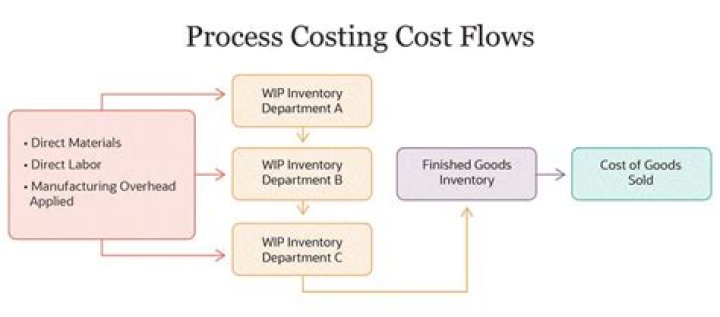

Cost Flow in Process Costing The typical manner in which costs flow in process costing is that direct material costs are added at the beginning of the process, while all other costs (both direct labor and overhead) are gradually added over the course of the production process.

How does process costing work?

Process costing is an accounting methodology that traces and accumulates direct costs, and allocates indirect costs of a manufacturing process. Costs are assigned to products, usually in a large batch, which might include an entire month’s production. Costs are averaged over the units produced during the period”.

What are the cost flows through a job cost system?

Overview of Cost Flows. The basic flow of costs in a job-order system begins by recording the costs of material, labor, and manufacturing overhead. a. Direct material and direct labor costs are debited to the Work In Process account.

What is a job in job order costing?

Job order costing is a costing method which is used to determine the cost of manufacturing each product. Job costing includes the direct labor, direct materials, and manufacturing overhead for that particular job.

Can a company use both job order costing and process costing?

Process costing and job order costing are both acceptable methods for tracking costs and production levels. Some companies use a single method, while some companies use both, which creates a hybrid costing system. The system a company uses depends on the nature of the product the company manufactures.

Which comes last in the flow of costs?

The process of the flow of costs begins with valuing the raw materials used in manufacturing. The flow of costs then moves to the work-in-process inventory. Conversely, if the company used the LIFO method, the last unit of raw materials purchased would be moved from inventory and charged to COGS as an expense.

What is a process cost summary?

Definition: A process cost summary is a production report that shows a department’s expenses, units produced, and costs allocated to the production units. In other words, this is a report that summaries all of the production activities of a department or process.

What comes first in the flow of costs?

The process of the flow of costs begins with valuing the raw materials used in manufacturing. The flow of costs then moves to the work-in-process inventory. The cost of the machinery and labor involved in production are added as well as any overhead costs.

How do process costing systems work?

A process costing system accumulates costs when a large number of identical units are being produced. A process costing system accumulates costs and assigns them at the end of an accounting period. At a very simplified level, the process is: Direct materials.

Which comes first in the flow of costs?

How are product costs assigned in a process costing system?

The primary difference between the two costing methods is that a process costing system assigns product costs—direct materials, direct labor, and manufacturing overhead—to each production department (or process) rather than to each job. Each production department has its own work-in-process inventory account when using process costing.

Which is the third step in the costing method?

The third step is to account for all the costs that are incurred during the whole production process. This is done by adding costs to each process to get an average individual cost per unit. Compared to the other costing methods available, this method uses quite a basic method to calculate these costs.

How does product cost flow through an account?

Identify how product costs flow through accounts using process costing. As products physically move through the production process, the product costs associated with these products move through several important accounts as shown back in Figure 4.1 “A Comparison of Cost Flows for Job Costing and Process Costing”.

What makes up the flow of costs in manufacturing?

Understanding Flow of Costs The process of the flow of costs begins with valuing the raw materials used in manufacturing. The flow of costs then moves to the work-in-process inventory. The cost of the machinery and labor involved in production are added as well as any overhead costs.