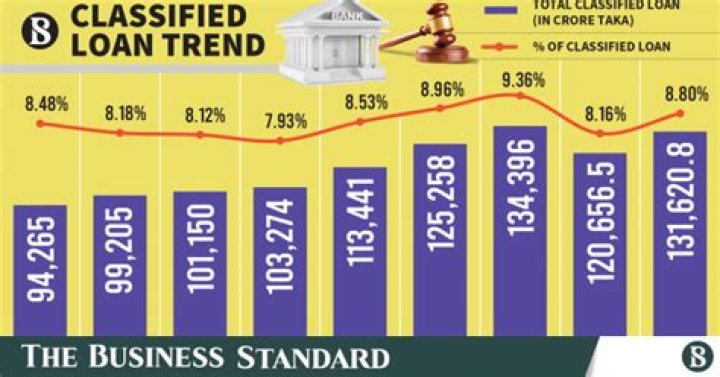

What is meant by classified loan?

James Craig

Published Feb 18, 2026

A classified loan is a bank loan that is in danger of default. Classified loans have unpaid interest and principal outstanding, but don’t necessarily need to be past due. As such, it is unclear whether the bank will be able to recoup the loan proceeds from the borrower.

What are the 3 classification of loans?

A loan is a sum of money that an individual or company borrows from a lender. It can be classified into three main categories, namely, unsecured and secured, conventional, and open-end and closed-end loans.

What is classified and unclassified loan?

Deeper definition Once a loan is classified, the bank can take steps to prepare for losses it expects to incur from the borrower’s non-payment. The bank may decide to change a loan’s status from classified to unclassified if the borrower misses a payment.

What are financing terms?

Financing terms can also relate to the specifics of a particular loan, mortgage, or credit facility. They would spell out the interest rate, due dates of payments, and number of payments anticipated.

How assets Loans are classified by banks?

Banks are required to classify non-performing assets further into the following three categories based on the period for which the asset has remained non-performing and the realisability of the dues: Sub-standard Assets. Doubtful Assets. Loss Assets.

How assets loans are classified by banks?

How do you classify an NPA account?

Sub-Classifications for Non-Performing Assets (NPAs)

- Standard Assets. They are NPAs that have been past due for anywhere from 90 days to 12 months, with a normal risk level.

- Sub-Standard Assets. They are NPAs that have been past due for more than 12 months.

- Doubtful Debts.

- Loss Assets.

Banks are required to classify nonperforming assets into one of three categories according to how long the asset has been non-performing: sub-standard assets, doubtful assets, and loss assets. Loss assets are loans with losses identified by the bank, auditor, or inspector that need to be fully written off.