What is Max contribution to Solo 401k?

Mia Ramsey

Published Mar 04, 2026

$57,000

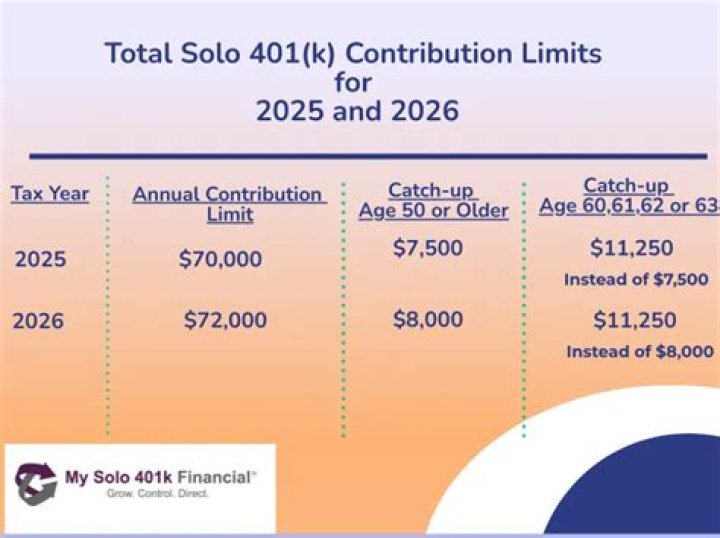

The total solo 401(k) contribution limit is up to $57,000 in 2020 and $58,000 in 2021. There is a catch-up contribution of an extra $6,500 for those 50 or older.

How do I correct excess Solo 401k contribution?

Tell your plan administrator you’ve made an “excess deferral.” The plan administrator will return the excess funds to you as a “corrective distribution.” They will also calculate and return the additional earnings (if any) and issue new paperwork that corrects the over-contribution.

What happens if you contribute too much to Solo 401k?

Handling excess earnings. Any income earned from the excess contribution will count on your tax bill, which is due the following April. You’ll receive a Form 1099-R at the end of the tax year in which the earnings were paid back to you.

How much can you put into a Solo 401k per year?

However, Solo 401k voluntary after tax contributions allow you to put up to $57,000 per year (or $63,000 per year if you are age 50 or older) into your retirement plan! Solo 401k voluntary after-tax contributions are a type of employee salary deferral contribution. They are not profit sharing employer contributions.

Is the Solo 401k a pre tax or after tax contribution?

The Solo 401k voluntary after-tax contribution is a type of employee salary deferral contribution. However, unlike the pre-tax or Roth employee contribution, the amount you can contribute can be much higher. While all Roth contributions are after-tax, not all after-tax contributions are Roth.

Can a employer match a Solo 401k contribution?

5) QRP-401k & Solo-401k Employer Matching Contributions. If the plan document permits, the employer can make matching contributions for an employee who contributes elective deferrals (for example, 50 cents for each dollar deferred).

Can a Solo 401k participant make a QRP contribution?

6) QRP-401k & Solo-401k Employer discretionary or nonelective contributions, often referred to as Solo 401k profit-sharing contributions. If the plan document permits, the employer can make contributions other than matching contributions for participants – regardless of whether or not they make elective deferrals.