What is included in non-recourse debt?

Mia Ramsey

Published Apr 01, 2026

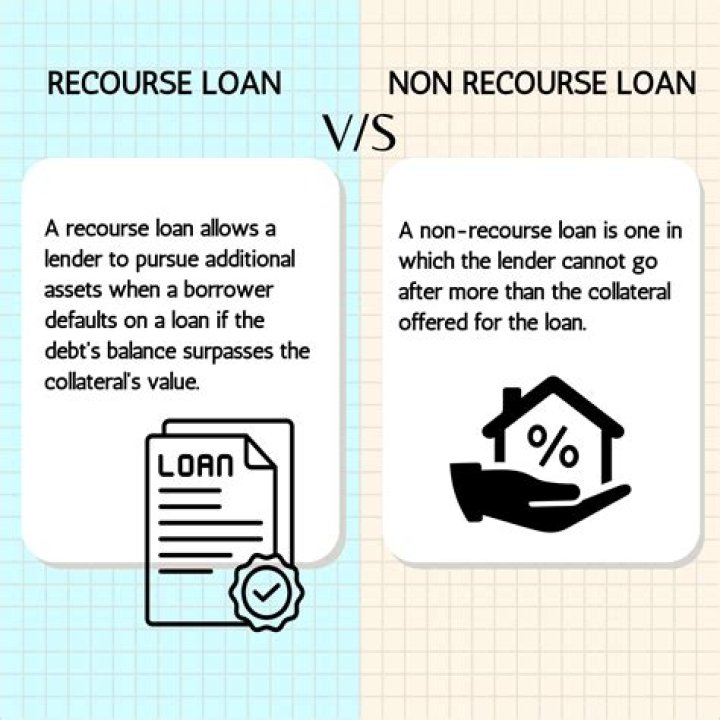

A nonrecourse debt (loan) does not allow the lender to pursue anything other than the collateral. For example, if a borrower defaults on a nonrecourse home loan, the bank can only foreclose on the home. The bank generally cannot take further legal action to collect the money owed on the debt.

What is a non-recourse transaction?

A non-recourse sale is a transaction between a buyer and a seller where the buyer accepts liability resulting from a defect in the asset sold. The term is generally used to describe the terms of a loan agreement, but it can also refer to a lender’s sale of bad debt to a third party, such as a debt collector.

Are non-recourse loans included in basis?

Nonrecourse liabilities can provide basis for distributions, but generally do not provide basis for purposes of the at-risk rules. Under an exception, a partner’s share of partnership debt that meets the definition of qualified nonrecourse financing does generate at-risk basis for that partner.

Are EIDL loans non-recourse?

Loans are non-recourse to the borrower. In addition to waiving any guaranty that might otherwise be required by the Small Business Act, the CARES Act specifically provides each loan is nonrecourse to the shareholders, members and partners of the borrower.

There are two types of debts: recourse and nonrecourse. A recourse debt holds the borrower personally liable. A nonrecourse debt (loan) does not allow the lender to pursue anything other than the collateral. For example, if a borrower defaults on a nonrecourse home loan, the bank can only foreclose on the home.

When a debt is nonrecourse?

Nonrecourse debt is debt that’s secured by collateral, which is the only asset a lender can take if you default on the debt. The lender can only use that collateral to cover the amount of debt owed. If the collateral doesn’t cover the amount of debt, the lender cannot seize any other property or money from you.

Which is the best definition of non recourse debt?

Non-Recourse Debt 1 Understanding Non-Recourse Debt. Because in many cases the resale value of the collateral can dip below the loan balance over the course of the loan, non-recourse debt is riskier to 2 Recourse vs. Non-recourse Debt. 3 Special Considerations. …

What’s the difference between recourse, nonrecourse and qualified?

The options are recourse, nonrecourse, and qualified nonrecourse debt. In order to further understand qualified nonrecourse debt, it is important to know the difference between recourse financial debt and non-recourse financial debt. Recourse debts are those which need to be paid one or another. Recourse loans have a collateral with them.

When do you take a non recourse loan?

Non-recourse debts are taken when mortgage is applied for in traditional terms. The only collateral the organization can hold against the person is the house itself. Nothing else can be held liable by the lender and in case of a loss, nothing else can be confiscated apart from the house to repay the loan.

When to use qualified nonrecourse debt in a partnership?

Qualified nonrecourse debt plays an important role when going through at basis and at risk limitations. Both these limitations define whether a partner in a business can deduct a loss or not in the partnership. In order to ensure that the basis calculations are correct, it is important to keep an eye on the K-1.