What is claimed depreciation?

Ava Robinson

Published Apr 09, 2026

Tax depreciation is the depreciation expense claimed by a taxpayer on a tax return to compensate for the loss in the value of the tangible assets. Examples include property, plant, and equipment. Tax authorities treat depreciation expenses as tax deductions.

When can depreciation be claimed?

109.1 Conditions for claiming depreciation – In order to avail depreciation, one should satisfy the following conditions : Condition 1 Asset must be owned by the assessee. Condition 2 It must be used for the purpose of business or profession. Condition 3 It should be used during the relevant previous year.

Why depreciation is claimed?

The Income Tax Officer also has the right to determine the proportionate part of the depreciation under Section 38 of the Act. Co-owners can claim depreciation to the extent of the value of the assets owned by each co-owner. You cannot claim depreciation on the cost of land. Depreciation is mandatory from A.Y.

When additional depreciation is allowed?

The rate of additional depreciation is 20% of the actual cost if asset is acquired and put to use for 180 days or more. The rate shall be 10% if period is less than 180 days, but a sum of 10% is allowed in the immediate next previous year….Depreciation for AY 2021-2022 under Income Tax Act, 1961.

| Ex showroom price | xxx |

|---|---|

| Add: Essential kit | xxx |

| Actual cost of car | xxx |

What if depreciation is not claimed?

If section 34 is not satisfied and the particulars are not furnished by the assessee his claim for depreciation under section 32 cannot be allowed. If the assessee has not claimed deduction of depreciation in any past year it cannot be said that it was notionally allowed to him. A thing is “allowed” when it is claimed.

When and how an additional depreciation should be claimed?

Additional depreciation to be allowed at 20 % of actual cost of new plant and machinery. However, if an asset is acquired and put to use for less than 180 days during the previous year, 50% of additional depreciation shall be allowed in year of acquisition and balance 50% would be allowed in the next year.

How an additional depreciation should be claimed?

According to this amendment, a provision has been inserted into the Section 32(1) (iia) which states that if an asset which has been acquired in the previous financial year and is being used for business purpose for less than 180 days in the previous year, then the additional depreciation permissible in that particular …

Can we claim less depreciation?

Lower Depreciation – Depreciation can be claimed at lower rate as per income tax act. But for the next year your wdv will be considered as reduced by the percentage of depreciation prescribed.

Who can claim accelerated depreciation?

Eligible businesses Businesses are eligible for the backing business investment – accelerated depreciation deduction if they have an aggregated turnover of less than $500 million in the year they are claiming the deduction. The deduction is available in the 2019–20 and 2020–21 income years.

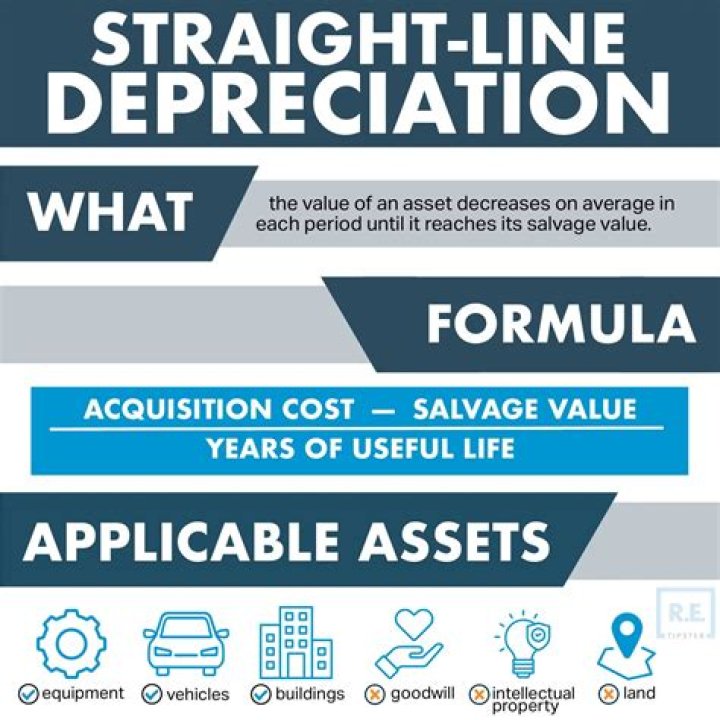

The concept of depreciation is used for the purpose of writing off the cost of an asset over its useful life. Depreciation is a mandatory deduction in the profit and loss statements of an entity and the Act allows deduction either in Straight-Line method or Written Down Value (WDV) method.

Can I claim depreciation on my personal car?

Let us see how. If you are self-employed and use your car for business purposes, you can claim depreciation on it which gets deducted from your taxable income. And it does not matter whether you buy a new car or a pre-owned car. The depreciation benefit is available for both.

Who can claim depreciation?

Conditions for Claiming Depreciation

- The asset must be owned by the assessee who claims the depreciation.

- The asset must have been used for the purpose of a business or profession carried on by the assessee.

- The asset should have been used during the relevant year in which depreciation allowance is claimed.

If the depreciation is not reduced while computing the income, the assessee would be claiming deduction on gross amount of income which would be more than that what the assessee is entitled to, and at the same time keeping WDV of its assets high resulting in higher claim of depreciation in subsequent years.

Can You claim depreciation on depreciating assets?

Claiming a deduction for depreciation Generally, you can claim a deduction for the decline in value of depreciating assets each year over the effective life. You can also ‘pool’ (or group) most depreciating assets and then claim depreciation for the pool, which is simpler than depreciating the individual assets.

Why was depreciation claimed on a car disallowed?

In the instant case, the depreciation claimed on the vehicles, i.e. cars and two-wheelers was disallowed by the AO on account of two reasons. Firstly, the assessee was not the owner of the assets, and secondly, the assessee failed to establish that the assets were used for the business.

Who is entitled for depreciation on vehicle registered in name of director?

The assessee has claimed depreciation in respect of certain vehicles which were registered in the name of Directors. The assessee claimed that it is the beneficial owner of the asset. The assessee further claimed that these assets were used only and exclusively for the business.

Can You claim depreciation on trademark even if not registered in Your Name?

In view of the above, it is held that the assessee was indeed eligible for depreciation in respect of the intangible asset by way of trademark. The Assessing Officer is, therefore, directed to grant the depreciation on the trademark. Claim depreciation on trademark even if not registered in your name.