What is bank adjustment deed in lieu?

Ava Robinson

Published Feb 24, 2026

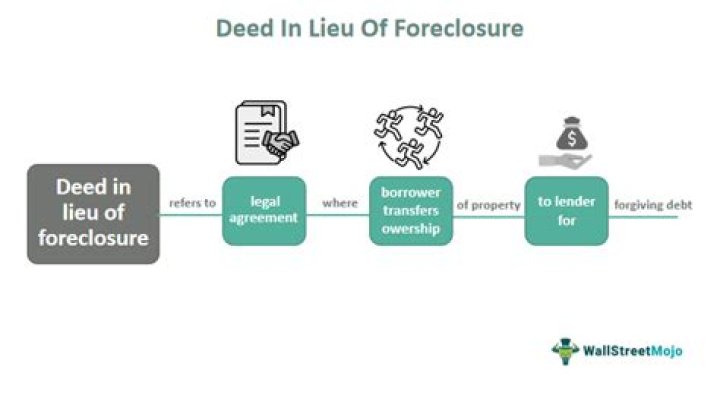

A deed in lieu of foreclosure, sometimes referred to as simply a “deed in lieu,” transfers a home’s title from the owner to the bank that holds the mortgage. The action is taken in lieu or instead of having the lender foreclose on the property.

How do you qualify for deed in lieu?

How Does a Deed in Lieu of Foreclosure Work?

- proof of income (generally two recent pay stubs or, if the borrower is self-employed, a profit and loss statement)

- recent tax returns.

- a financial statement, detailing monthly income and expenses.

- bank statements (usually two recent statements for all accounts), and.

Is deed in lieu a good idea?

Your credit will still take a hit: While a deed in lieu arrangement won’t harm your credit as drastically as a foreclosure, you can still expect your score to drop. You also won’t be able to easily get another mortgage if you have a deed in lieu on your credit report.

Why are lenders not accepting deed in lieu?

It’s important to remember that your lender has no obligation to accept a deed in lieu agreement. Some of the reasons why a lender might reject a deed in lieu include: A depreciated home value: If the value of your home has gone down, you might owe more on your loan than your home is worth.

Is there a waiting period for deed in lieu of foreclosure?

If a full foreclosure takes place, a seven-year waiting period is required. And while short sales require listing a home and trying to find a buyer to get out of foreclosure, the deed in lieu process skips that step.

Which is better deed in lieu of foreclosure or short sale?

And while foreclosure will almost certainly hurt your credit score, a deed in lieu of foreclosure tends to be viewed more favorably by future lenders, Wilson says. It’s rated on par with a short sale by most creditors who are reviewing a borrower’s ability to purchase a future home.

Can a subordinate lien holder sign a deed in lieu of foreclosure?

It can be difficult to get subordinate lien holders to agree to a deed in lieu of foreclosure or short sale. For this reason, the borrower often needs to provide some type of financial incentive.