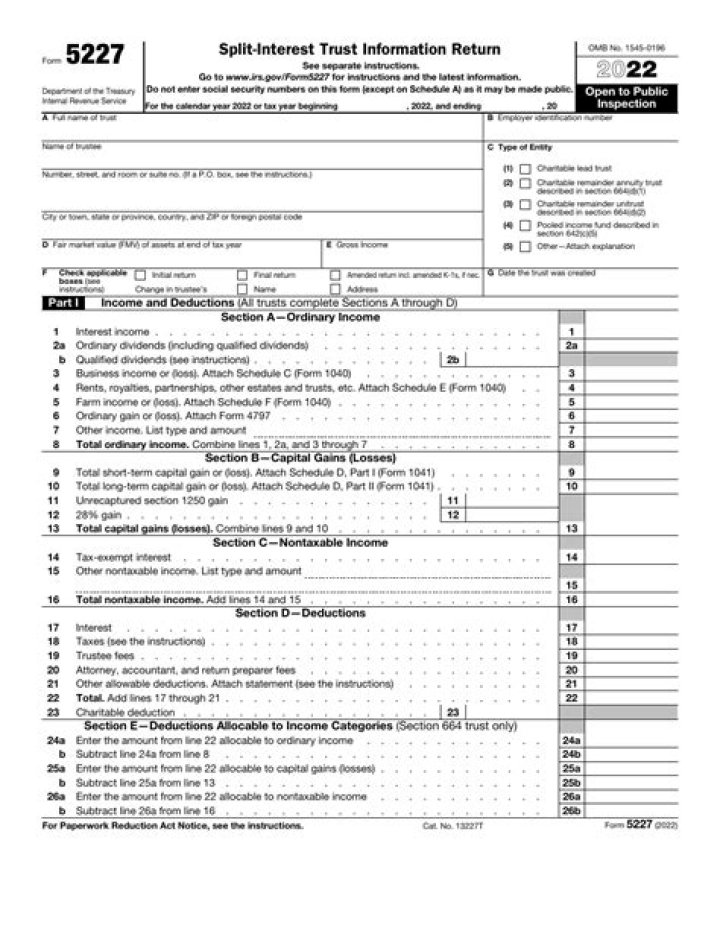

What is an IRS form 5227?

Henry Morales

Published Apr 03, 2026

Use Form 5227 to: Report the financial activities of a split-interest trust. Provide certain information regarding charitable deductions and distributions of or from a split-interest trust. Determine if the trust is treated as a private foundation and subject to certain excise taxes under Chapter 42.

How do you close a charitable remainder trust?

Three Ways to Terminate a CRT Early

- Donating all or an undivided fractional portion of the income interest to the charitable remainder beneficiary.

- “Cashing in” all or a portion of the income interest.

- Selling to an unrelated third party.

How do I extend my 5227?

Use Form 8868 to request an automatic extension of time to file. The request for an automatic extension must be filed by the due date of the return.

Are distributions from a CRUT taxable?

Is income tax imposed on the distributions and who pays it? CRTs are exempt from income tax. The CRT assumes the grantor’s adjusted cost basis and holding period in the property.

How do I end my CRUT early?

Perhaps the simplest method of terminating a CRT early is to transfer all trust income interests to the tax-exempt organization(s) entitled to the CRT remainder. Under most states’ statutes and their common law, this “merges” the CRT beneficial interests.

Is a CRUT a split interest trust?

A charitable remainder trust is a “split interest” giving vehicle that allows you to make contributions to the trust and be eligible for a partial tax deduction, based on the CRT’s assets that will pass to charitable beneficiaries.

Is CRUT income taxable?

The annuity paid from the CRUT is taxable to the person receiving the payment. The annuity is taxed in the so-called “Worst-In, First-Out” (WIFO)method. Roughly, the annuity is taxed in the following order of the CRUTs income: ordinary income, capital gain, other income, and trust corpus.

How are unitrust distributions taxed?

Distributions from a charitable remainder unitrust are taxed to income recipients based on what is known as the “four-tier system” of taxation. Conversely, if you transfer tax-exempt bonds and the trustee continues to hold them, your income distributions would be tax-exempt.

What is the due date for Form 5227?

April 15, 2021

When To File File Form 5227 for calendar year 2020 by April 15, 2021. In the case of a final short-year period, the return is due by the 15th day of the 4th month following the date of the trust’s termination.

Can I electronically file Form 5227?

Form 5227, Split-Interest Trust Information Return, cannot be e-filed. The form is available in the 1041 fiduciary return by completing applicable screens on the 5227 tab. The presence of a Form 5227 does not prevent e-filing a 1041, but the 5227 is not transmitted with the 1041.

CRTs are exempt from income tax. The CRT assumes the grantor’s adjusted cost basis and holding period in the property. Distribution amounts in excess of the above items of income are treated as non-taxable return of principal.

What is a section 664 trust?

Charitable Remainder Trusts. Fourth, as a distribution of trust corpus. For purposes of this section, the trust shall determine the amount of its undistributed capital gain on a cumulative net basis.

What are the general instructions for form 5227?

General Instructions Purpose of Form Use Form 5227 to: •Report the financial activities of a split-interest trust, •Provide certain information regarding charitable deductions and distributions of or from a split-interest trust, and

What kind of trust can use form 5227?

Certain parts of Form 5227 apply exclusively to a particular type of split-interest trust (such as a charitable remainder trust, also referred to as a “section 664 trust”).

Do you have to include NIMCRUT in charitable remainder?

Charitable remainder unitrusts must include any unitrust amounts applicable to prior periods that are unpaid but required to be paid as of the valuation date, since such amounts reduce the net FMV of the trust’s assets. However, don’t include any make-up amount for a NIMCRUT.

What is a net income makeup Charitable Remainder Unitrust?

A Net-Income Makeup Charitable Remainder Unitrust (NIMCRUT) is a charitable remainder unitrust that allows payment of the unitrust amount to be deferred in years when the unitrust amount exceeds trust income, with the deferred distributions being made up in a later year when the trust has sufficient income.