What is an apportionment formula?

Andrew Mclaughlin

Published Mar 05, 2026

Apportionment formulas are designed to allocate to a taxing state, for tax purposes, a share of a company’s income that corresponds to its business activity in the state. State formulas use one or more factors to determine each company’s overall income apportionment percentage.

What is state apportionment information?

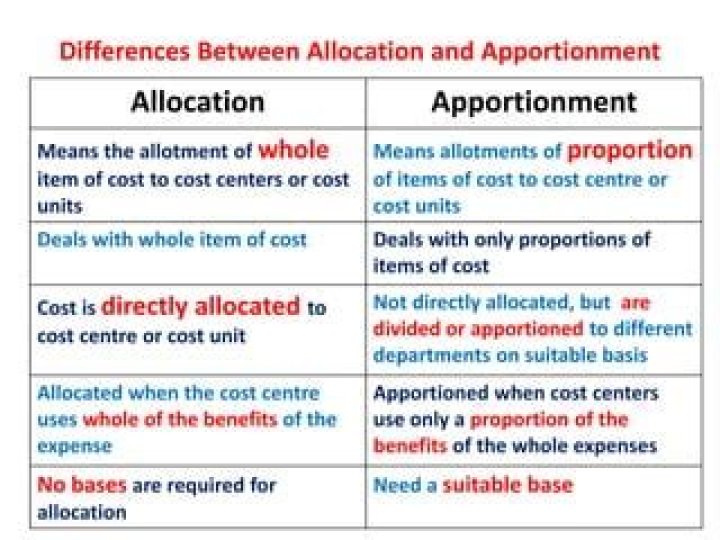

As noted, apportionment refers to the manner in which income is divided between various taxing jurisdictions. All your income gets a portion to that one state or get sourced that one state. That state gets to tax 100% of your income.

Which states use single factor apportionment?

By the end of 1995, five states had enacted a single sales factor formula for manufacturers — Iowa, Massachusetts, Missouri, Nebraska, and Texas. (Massachusetts implemented a sales-only formula immediately for defense contractors and phased it in between 1996 and 2000 for other manufacturers.)

What are the three most common types of state apportionment formulas?

Trades or businesses that derive more than 50% of their gross receipts from QBA must use the three factor formula consisting of property, payroll, and single-weighted sales factor to apportion business income to California.

How is property apportionment calculated?

The apportionment percentage is determined by adding the taxpayer’s receipts factor (as described in Section 3 of this article), property factor (as described in Section 4 of this article), and payroll factor (as described in Section 5 of this article) together and dividing the sum by three.

How do you calculate apportionment?

Calculating apportionment for income

- Identify your gross income for the quarter.

- Calculate your company’s book value.

- Divide your gross income figure by the number of days in the relevant quarter.

- Multiply this number by the number of days in the year.

- Finally, divide your final figure by the value of your business.

What is the best apportionment method?

These methods are some of the most frequently used apportionment methods, although readers might know them by different names. The Jefferson method is also known as the greatest divisor method, the d’Hondt method, and the Hagenbach-Bischoff method.

How does New York state calculate business apportionment?

Under these rules, taxpayers would apportion their total business income and business capital by a business apportionment fraction, the numerator of which is the sum of all New York business receipts and the denominator of which would be their everywhere receipts.

What was the Massachusetts formula for tax apportionment?

The formula placed an equal weight on three factors: group sales, payroll, and property within each jurisdiction. Out of the forty-four states (plus one more jurisdiction, the District of Columbia) which imposed a corporate income tax in 1978, all but Iowa used the Massachusetts Formula.

How to calculate the apportionment of a quarter?

Divide the gross income figure from Step 2 by the number of days in the quarter from Step 1. Continuing the same example, $110,000 / 90 = 1,222.22. Multiply the figure from Step 4 by the number of days in a year. This number is typically 365 unless it is a leap year, when you’d use 366. Continuing the same example, 1,222.22 x 365 = 446,111.11

What are the rules for apportionment in a combined report?

Section 4-1.2 of the draft regulations provides rules for apportionment among members filing a combined report. For purposes of a combined report, “taxpayer” means all corporations included in a combined report, regardless of whether the individual members are subject to tax.