What is a qualified report draft a qualified audit report?

John Thompson

Published Feb 17, 2026

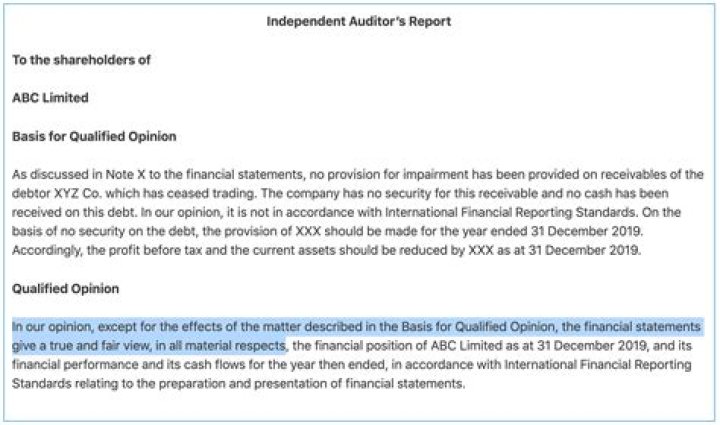

The simple meaning of qualified audit report is that the accounting information that presents in the financial statements is not correct. In the qualified audit report, there is a qualified audit opinion that expresses by auditors and stating the reason why the qualified opinion is expressed.

How do you report qualification in audit report?

Qualified Audit Report: A qualified opinion shall be expressed as being subject of or except for the effects of the matter to which the qualification matters. If the accounting standards issued by Institute of Chartered Accounts of India is not followed by the company the auditor may qualify his report.

Is a qualified audit report bad?

A qualified opinion means that your financial statements are auditable but have financial or compliance issues that materially affect one or more funds within the overall financial statement. A disclaimed opinion is very bad.

What is the difference between a qualified and unqualified audit opinion?

A qualified opinion is a reflection of the auditor’s inability to give an unqualified, or clean, audit opinion. An unqualified opinion is issued if the financial statements are presumed to be free from material misstatements. A qualified opinion is still acceptable to most lenders, creditors, and investors.

How do you know if an audit is unqualified?

For an unqualified report, the auditor has concluded that most financial matters are dealt with correctly—although there may be some outstanding minor issues. In contrast, an auditor’s report is qualified for reasons such as limited scope in the auditor’s work or if there are issues concerning the accounting policies.

What is the difference between unqualified and qualified audit report?

Who is the owner of audit working papers?

Ownership of Audit working papers “The working paper belongs to the auditor not to the client, as the auditor is an independent contractor and not the agent of the client”. “The working papers prepared by the auditor are the property of the auditor”. Thus, the working papers are the property of the auditor.