What is a PTP loss carryforward?

Sarah Duran

Published Apr 05, 2026

If you have an overall loss (but did not dispose of your entire interest in the PTP to an unrelated person in a fully taxable transaction during the year), the losses are allowed to the extent of the income, and the excess loss is carried forward to use in a future year when you have income to offset it.

Are PTP losses deductible?

A disallowed loss from a PTP is carried forward and allowed as a deduction in a tax year when the PTP has net income or when the taxpayer disposes of his or her entire interest in the PTP.

Are PTP losses passive?

IRS rules treat an overall loss from a publicly traded partnership (PTP) as passive and an overall gain from a PTP as nonpassive.

What is a PTP loss?

The losses a PTP generated that annually flow through to the partner are by definition passive losses, the deduction of which are severely limited. 28. The flowthrough passive losses cannot be deducted until that PTP generates passive income or the interest is disposed of in a taxable transaction.

When does the ordinary loss on a PTP become taxable?

The ordinary loss would not be currently deductible by the partner until the PTP generated passive income or was completely disposed of in a taxable transaction, but the interest income would be taxable immediately.

Can a loss be carried forward on a tax return?

Loss under the head “Income from house property” can be carried forward even if the return of income/loss of the year in which loss is incurred is not furnished on or before the due date of furnishing the return, as prescribed under section 139(1).

Can a loss be carried forward to next assessment year?

Balance Losses if any, shall be carried forward to next Assessment Year. v) However, Losses from other heads of Income (Except capital Gains) can be set off against House Property Income without any restrictions. For Example: Losses from Normal business Rs 10 Lacs can be adjusted against house Property Income of Rs 8 Lacs.

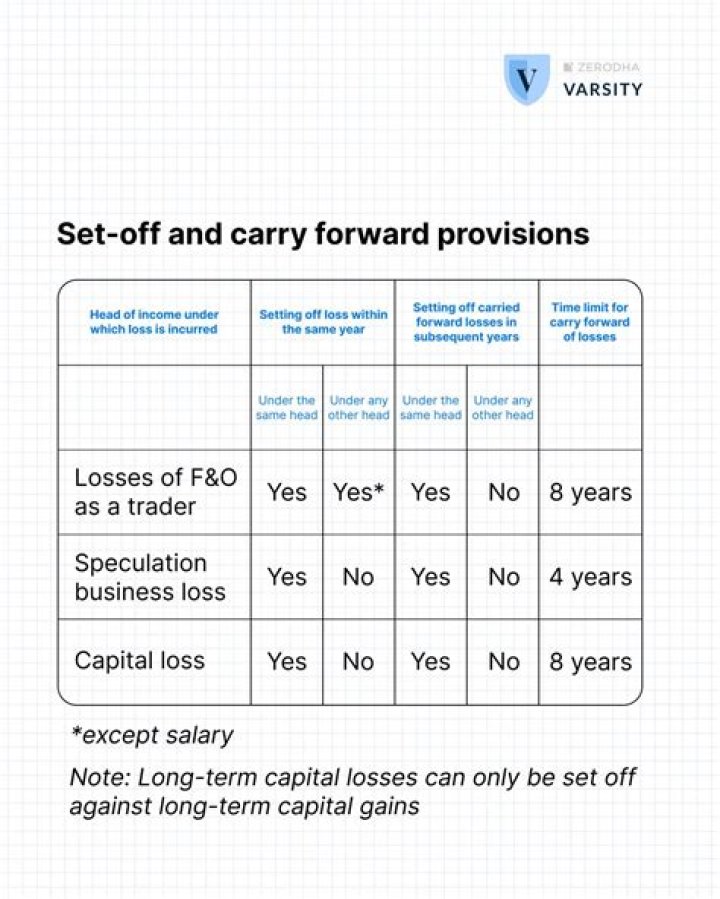

Can a loss from speculative business be carried forward?

Loss from speculative business can be carried forward only if the return of income/loss of the year in which loss is incurred is furnished on or before the due date of furnishing the return, as prescribed under section 139(1). Such loss can be carried forward for four years immediately succeeding the year in which the loss is incurred.