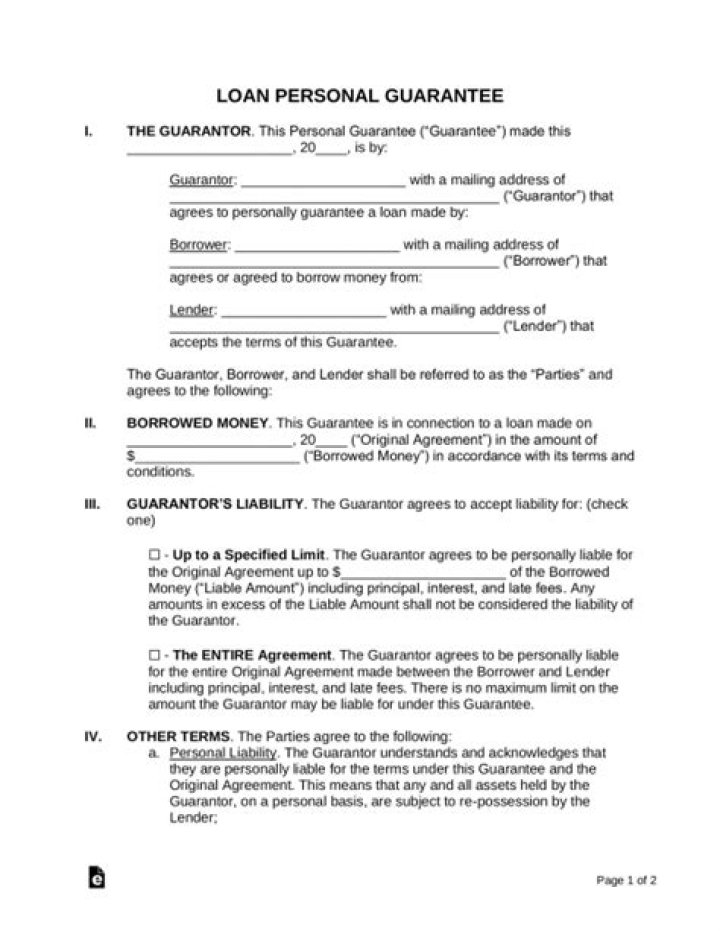

What is a personal guarantee on a line of credit?

John Thompson

Published Mar 19, 2026

A personal guarantee is an individual’s legal promise to repay credit issued to a business for which they serve as an executive or partner. Personal guarantees help businesses get credit when they aren’t as established or have an inadequate credit history to qualify on their own.

Is guarantee required for personal loan?

When a person applies for a Personal Loan, many banks ask for a guarantor. He/she is not only a witness or someone who proves the authenticity of the borrower, but is also someone who guarantees that the borrower will repay the loan.

Why do banks ask for personal guarantees?

Most lenders, including online lenders like OnDeck, require personal guarantees. It reduces the lender’s risk associated with the loan because it gives the lenders the right to pursue a borrower’s personal assets if your business fails to repay the debt.

How enforceable is a personal guarantee?

A personal guaranty is not enforceable without consideration In fact, no contract is enforceable without consideration. A personal guaranty is a type of contract. A contract is an enforceable promise. The enforceability of a contract comes from one party’s giving of “consideration” to the other party.

How do I get rid of a personal guarantee?

Unless a business is a sole proprietorship, personal guarantees can only be discharged by filing an individual bankruptcy. A business bankruptcy will not eliminate a personal guarantee. Likewise, the Chapter 13 co-debtor stay only applies to consumer debts and personal guarantees are usually considered business debts.

How do I cancel a guarantor agreement?

How Do I Stop Being A Tenant Guarantor?

- The landlord allows the guarantor to surrender their legal obligations as a guarantor.

- If the Deed of guarantee contains a termination provision (allowing the guarantor to withdraw on say two months’ notice)- the provision can allow the termination during the fixed term.

What happens if I can’t pay back SBA loan?

Default on the SBA Loan First, the lender will seek payment from the business for the outstanding balance of the loan. However, if the business cannot pay the full amount, the lender will foreclose on the collateral pledged by the business.

What happens if you don’t pay your SBA loan back?

The lender has the right to seize the assets the borrower used as collateral to back the loan. If you default and the lender takes a loss on the loan, it submits the loss to the SBA to honor its guarantee. The SBA guarantees up to 85% on loans of $150,000 and less, and up to 75% on loans over $150,000.

Can SBA loans be non recourse?

SBA has no recourse (or will demand compensation or payment) against individuals, shareholders, members, or partners of an eligible recipient unless the ‘covered loan’ proceeds are used for unauthorized purposes (see above). There are no personal guarantee requirements and no collateral requirements for ‘covered loans.

How do you get out of a personal guarantee?

The financial institution is not obligated to grant a Release of Personal Guarantee. In the event the Release of Personal Guarantee is not obtained, a most frequent way to receive the release is to pay off the business loan or refinance the business through a private equity firm.