What is a 1256 gain or loss?

Sarah Duran

Published Mar 04, 2026

A Section 1256 contract specifies an investment made in a derivatives instrument whereby if the contract is held at year-end, it is treated as sold at fair market value at year-end. The implied profit or loss from the fictitious sale are treated as short- or long-term capital gains or losses.

Do you pay capital gains on options?

If you’ve held the stock or option for less than one year, your sale will result in a short-term gain or loss, which will either add to or reduce your ordinary income. Options sold after a one year or longer holding period are considered long-term capital gains or losses.

Are options 1256?

A 1256 Contract, as defined in section 1256 of the U.S. Internal Revenue Code, is any regulated futures contracts, foreign currency contracts, non-equity options (broad-based stock index options (including cash-settled ones), debt options, commodity futures options, and currency options), dealer equity options, dealer …

Can losses be carried back?

Taxpayers can carry back NOLs, including non-farm NOLs, arising from tax years beginning in 2018, 2019, and 2020 for 5 years. See section 172(b)(1)(D)(i). Special election for farming losses for 2018, 2019, and 2020.

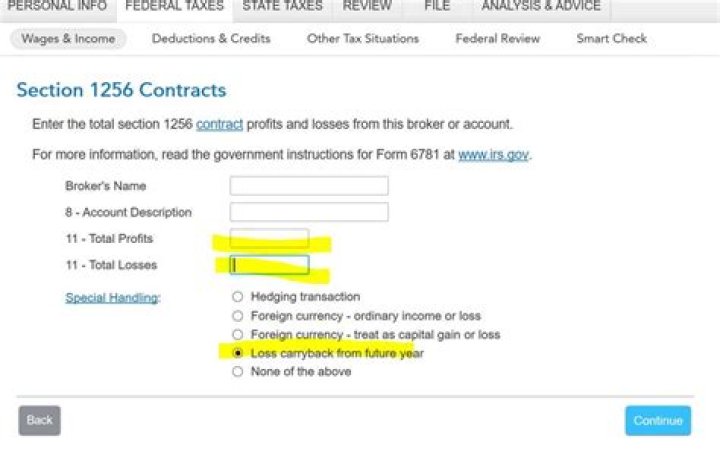

How to report gains and losses on Section 1256 Contracts?

Use Form 6781 to report gains/losses on section 1256 contracts under the mark-to-market rules and under section 1092 from straddle positions. Use Form 6781 to report: Any gain or loss on section 1256 contracts under the mark-to-market rules. Gains and losses under section 1092 from straddle positions.

Can you carry a Section 1256 loss back 3 years?

If you have a net section 1256 contracts loss for 2019, you can elect to carry it back 3 years. Corporations, partnerships, estates, and trusts aren’t eligible to make this election. Your net section 1256 contracts loss is the smaller of: • The

What do you need to know about Section 1256?

Section 1256 contracts and straddles are named for the section of the Internal Revenue Code that explains how investments like futures and options must be reported and taxed. Under the Code, Section 1256 investments are assigned a fair market value at the end of the year.

How is implied profit or loss treated under Section 1256?

The implied profit or loss from the fictitious sale are treated as short- or long-term capital gains or losses. Section 1256 is used to prevent manipulation of derivatives contracts, or their use thereof, to avoid taxation.