What happens when you work as a 1099 employee?

Mia Ramsey

Published Feb 24, 2026

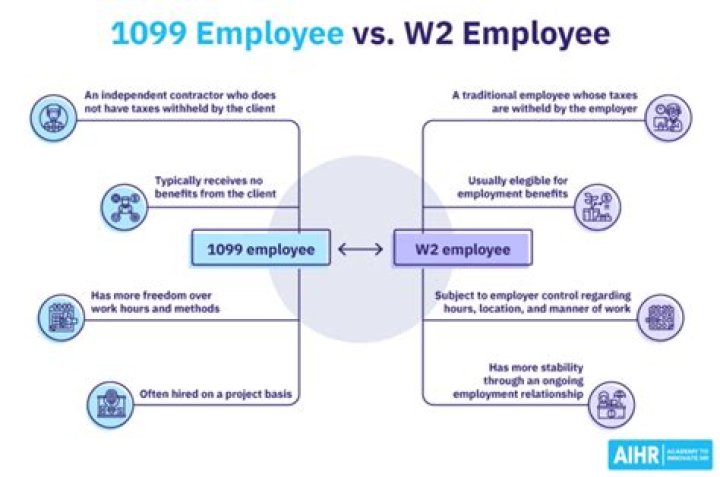

As it says on the information above, when you work as a 1099 employee, you’re not an employee. Instead, you’re considered an independent contractor. As an independent 1099 worker, you can enjoy the advantages of setting your own price, working around your own schedule and controlling how you meet your obligations to your clients.

Why do I get a 1099 instead of a W-2?

Instead of being an employee of the company, you are employed by your own business, or “self-employed.” You’ve probably received a 1099 tax form, instead of a W-2. Many people are true independent contractors – for example, independent electricians or accountants who have many clients with whom they have business relationships.

Do you call someone a 1099 employee or independent contractor?

To call somebody a “1099 employee” is misleading: To the person or company you’re working for under a 1099, you’re not an employee. Instead, you’re considered an independent contractor. Your income throughout the year is reported to the IRS with Form 1099-MISC.

What do I need to know about 1099 MISC?

If you’re an independent contract worker, you’ll receive Form 1099-MISC from each business that paid you at least $600. Even if a business doesn’t send you this form, you’re still required to report 100% of your earnings to the IRS. 1099-NEC. This form is brand new for 2020 and stands for Nonemployee Compensation.

How to report a company bonus received on a 1099-MISC?

[Probably should have been box 3] You received this form instead of Form W-2 because the payer did not consider this to be reportable as regular wages [or other reasons] and did not withhold income tax or social security and Medicare tax. Click the “tools” lower left and then in the pop up use ” ‘topic search” and type 8919 then click “go”

Who is responsible for paying taxes on a 1099 MISC?

Their employer pays the other half. For the income reported on a Form 1099-MISC, however, no tax has been withheld by the party that paid the self-employed individual for work performed. The self-employed person is responsible for paying both the employer and employee portions of payroll taxes.