What happens to depreciation when you sell a business?

Sarah Duran

Published Apr 05, 2026

Depreciation spreads the item’s cost out over its life, simulating its gradual deterioration or obsolescence. When you sell an a depreciated asset, the proceeds could be taxable if you sell it for more than its depreciated value.

How do you calculate depreciation on a case of sale of assets?

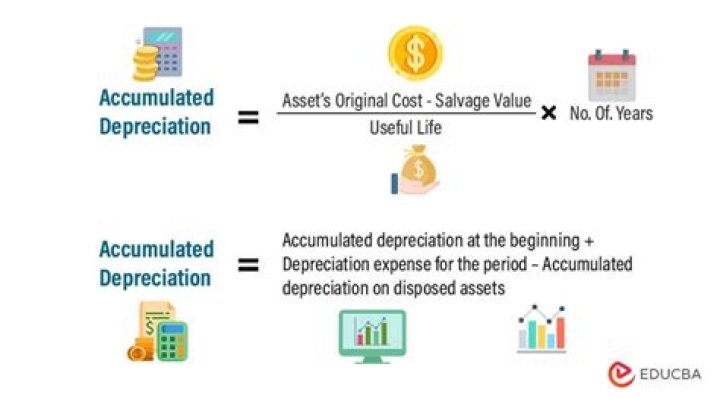

CALCULATION OF DEPRECIATION

- WDV of an asset = Actual cost to the assesse – All depreciation actually allowed to him (included unabsorbed depreciation, if any)

- WDV of Block of Assets.

If you sell that piece of equipment before you get to the end of its expected useful life, you’ll lose some of the 179 depreciation deduction. If you start using a business asset more than 50 percent of the time for personal use, the IRS will also take back some of your 179 deduction.

Can a company remove a fully depreciated asset?

A company should not remove a fully depreciated asset from its balance sheet. The company still owns the item, and needs to report this ownership to stakeholders. Companies can include a financial note or disclosure indicating the full depreciation of the asset.

Can a fully depreciated asset be reported on the balance sheet?

Financial Reporting. A company should not remove a fully depreciated asset from its balance sheet. The company still owns the item, and needs to report this ownership to stakeholders. Companies can include a financial note or disclosure indicating the full depreciation of the asset.

What’s the difference between fixed assets and depreciation?

Fixed assets represent items a company will use for several years. Depreciation is the expense that companies report for using the asset. Fully depreciated assets indicate a company used an item until there was no financial value left.

How does depreciation affect profit on sale of assets?

If the company plans to sell out the building at the current market value, the entire accumulated depreciation would be written-off against the building & the gain on the sale of assets will be credited to profit & loss a/c as “gain on sale of assets” thus inflating the current years profit by the gain amount.