What happens if you file a tax return without a 1099-R?

Sarah Duran

Published Feb 09, 2026

If you file a tax return without a 1099-R you received, your information will not match the records the IRS has. In the case of a form such as a W2 or a 1099-R, this will usually result in the IRS sending you a letter requesting the omitted form. In some cases, the IRS may send you an adjustment letter in addition to the request for your 1099-R.

Can a 1099-R be audited by the IRS?

When a 1099-R you receive is not reported on your original tax return, the IRS may conduct an audit, but this is not always a standard procedure performed in every such instance.

Do you need to report a 1099-R rollover?

Yes, you should request a Form 1099-R for this rollover before you file your tax return. You will need to report the distribution even though it was rolled over. June 7, 2019 3:10 PM Have contacted the indirect IRA rollover destination Vanguard; they tell me they send out a form 5498 in May, confirming the rollover.

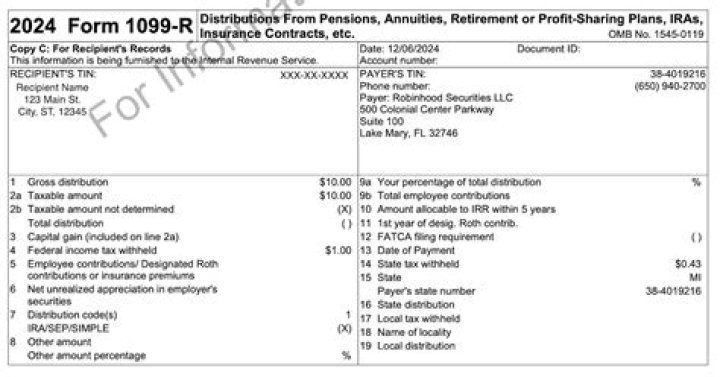

Is there a copy of the 2018 Form 1099-R?

2018 Form 1099-R Attention: Copy A of this form is provided for informational purposes only. Copy A appears in red, similar to the official IRS form. The official printed version of Copy A of this IRS form is scannable, but the online version of it, printed from this website, is not. Do not

Do you have to file Form 1099 for worthless property?

If you are distributing worthless property only, you are not required to file Form 1099-R. However, you may file and enter 0 (zero) in boxes 1 and 2a and any after-tax employee contributions or designated Roth contributions in box 5.

What to do with Form 1099 and form 4852?

The IRS will also send you a Form 4852, Substitute for Form W-2, Wage and Tax Statement, or Form 1099-R, Distributions From Pensions, Annuities, Retirement or Profit-Sharing Plans, IRAs, Insurance Contracts, etc., along with a letter containing instructions for you.

When do corrective distributions have to be reported on Form 1099?

Corrective distributions must include earnings through the end of the year in which the excess arose. These distributions are reportable on Form 1099-R and are generally taxable in the year of the distribution (except for excess deferrals under section 402(g)).