What happens if I take a lump sum from my 401k?

Mia Ramsey

Published Feb 24, 2026

Also keep in mind that if you take a lump sum and don’t roll it over into an IRA before age 59 1/2, you’ll pay an additional penalty. * What Do You Need to Do to Take the Lump Sum?

What should I do with my deceased spouse’s 401k?

If you are a beneficiary of your deceased spouse’s IRA or 401 (k), you can: Withdraw all the money now (and pay whatever income tax is due). Roll over the account into your own traditional or Roth IRA—an existing account or one you open now. Put the money in an “Inherited IRA.”

When do I have to disclaim from my spouse’s 401k?

You must disclaim within nine months after the death of your spouse and before you take possession of the funds. Once you disclaim, you can’t get the money back if change your mind.

What happens when a spouse inherits an IRA or 401k?

Inheriting the money in someone’s IRA or 401 (k) is different from inheriting other property. The IRS has detailed rules about these retirement plans, and if you don’t follow them, you risk losing flexibility and tax benefits. Spouses get special treatment when they inherit retirement accounts; they get more options than do other beneficiaries.

When to take a lump sum retirement distribution?

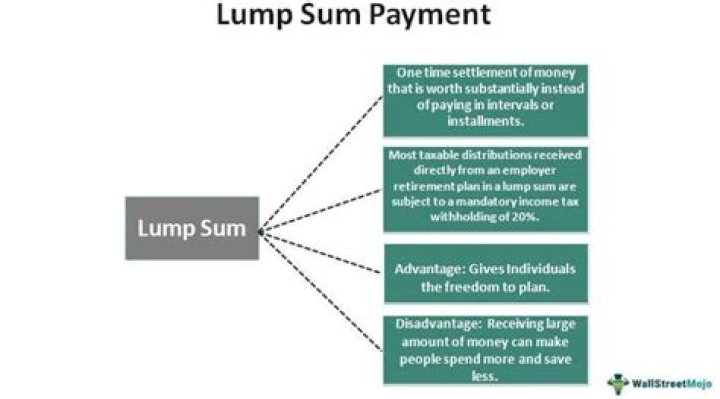

When making a decision to transfer a qualified retirement plan, taking a lump-sum distribution is usually one of at least three choices, including a rollover, partial distribution or keeping the benefit in the current account indefinitely or as long as the plan or account custodian allows.

What does it mean to get a lump sum pension payment?

Updated July 25, 2019. A lump-sum distribution is a financial term that usually refers to an election to receive a 401(k) plan or pension benefit as a one-time payment for the entire balance.

What are the tax consequences of a lump sum distribution?

1 A lump-sum distribution is the payment of the full balance of a 401 (k), pension, or another retirement account within a single tax year. 2 This can be taken as a cash payout or rolled over into another retirement account. 3 Tax consequences can be significant but will vary depending on the lump-sum recipient’s age and how they take the payout.