What gets closed off to retained earnings?

Emma Jordan

Published May 17, 2026

In accounting, we often refer to the process of closing as closing the books. Only revenue, expense, and dividend accounts are closed—not asset, liability, Common Stock, or Retained Earnings accounts.

What are end of year retained earnings?

Retained earnings are like a running tally of how much profit your company has managed to hold onto since it was founded. They go up whenever your company earns a profit, and down every time you withdraw some of those profits in the form of dividend payouts.

Why would a company have negative retained earnings?

Negative retained earnings are what occurs when the total net earnings minus the cumulative dividends create a negative balance in the retained earnings balance account. Negative retained earnings often show that a company is experiencing long-ter losses and can be an indicator of bankruptcy.

In accounting, we often refer to the process of closing as closing the books. Only revenue, expense, and dividend accounts are closed—not asset, liability, Common Stock, or Retained Earnings accounts. Closing the Dividends account—transferring the debit balance of the Dividends account to the Retained Earnings account.

Do you close distributions to retained earnings?

Distribution accounts close to the retained earnings account. Monthly activity is captured in the distribution account and fed into the retained earnings account at the end of the accounting period.

Why do s Corp have a retained earnings account?

Furthermore, an S Corp that has this type of accounting system shouldn’t have any retained earnings. But the retained earnings account allows the S Corp to keep track of the amount of any undistributed income.

What are the closing entries on the statement of retained earnings?

The closing entries are the journal entry form of the Statement of Retained Earnings. The goal is to make the posted balance of the retained earnings account match what we reported on the statement of retained earnings and start the next period with a zero balance for all temporary accounts.

Do you have to restate beginning retained earnings?

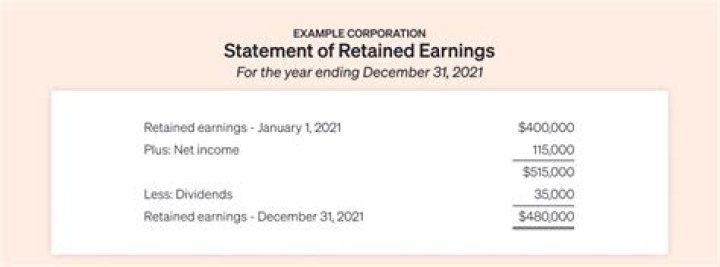

+ Beginning retained earnings + Net income during the period – Dividends paid = Ending retained earnings It is also possible that a change in accounting principle will require that a company restate its beginning retained earnings balance to account for retroactive changes to its financial statements.

Are there any contractual restrictions on retained earnings?

These contractual or voluntary restrictions or limitations on retained earnings are retained earnings appropriations. For example, a loan contract may state that part of a corporation’s $100,000 of retained earnings is not available for cash dividends until the loan is paid.