What does liquidated partnership interest mean?

Mia Ramsey

Published Mar 02, 2026

A liquidating distribution terminates a partner’s entire interest in the partnership. A current distribution reduces a partner’s capital accounts and basis in his interest in the partnership (“outside basis”) but does not terminate the interest.

How do I report installment sale of partnership interest?

Reporting Installment Sale Income Generally, you will use Form 6252 to report installment sale income from casual sales of real or personal property during the tax year. You will also have to report the installment sale income on Schedule D (Form 1040), Form 4797, or both.

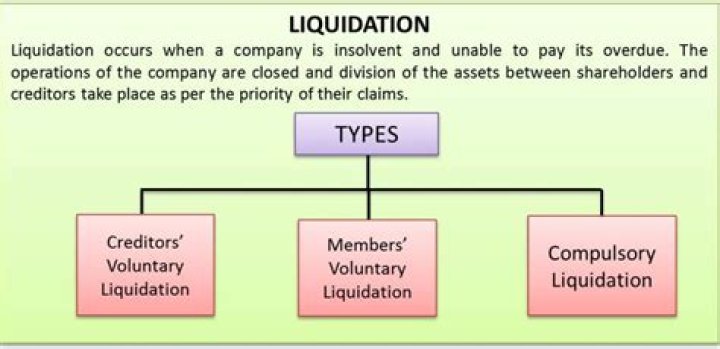

How do you liquidate a partnership?

The following four accounting steps must be taken, in order, to dissolve a partnership: sell noncash assets; allocate any gain or loss on the sale based on the income-sharing ratio in the partnership agreement; pay off liabilities; distribute any remaining cash to partners based on their capital account balances.

What is tax treatment of redemption of partnership interest?

The tax treatment of the redemption of a partnership interest involving deferred payments is more advantageous to the retiring partner than the sale of the partnership interest. A retiring partner receiving redemption payments in more than one year is generally able to fully recover his basis before any gain is recognized.

When does a partner purchase a partnership interest?

When a partner purchases a partnership interest from another partner, the transferee partner’s purchase price becomes the initial outside basis. When a partnership interest is acquired by gift, the transferee partner’s basis generally equals the donor’s basis.

How to keep track of a partnership interest?

Keeping Track of Basis in a Partnership Interest. When a partner purchases a partnership interest from another partner, the transferee partner’s purchase price becomes the initial outside basis. When a partnership interest is acquired by gift, the transferee partner’s basis generally equals the donor’s basis.

How does a liquidation of a partnership interest work?

The liquidation of a partner’s entire partnership interest can take various forms, including payment made by the partnership to the retiring partner in complete redemption of the partner’s interest or a sale of such interest to the remaining partners.